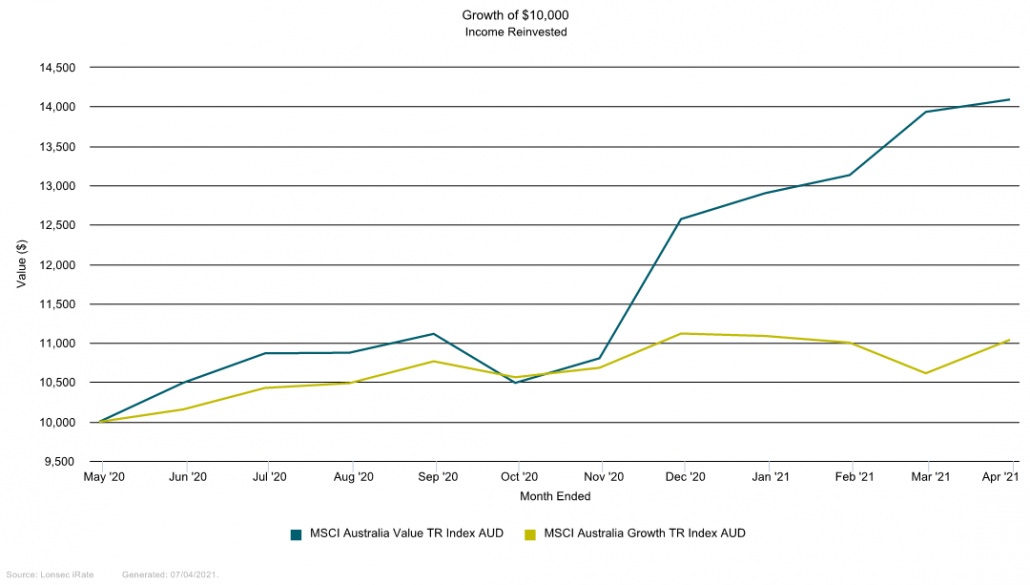

The rotation out of growth into value sectors continued over the March quarter as the economic recovery began to materialise with a lower unemployment rate contributing to stronger growth. Unless some unforeseen tail risk event occurs, it is expected that business and consumer confidence will rise, providing a clear indication of ‘normal’ conditions returning in the not-too-distant future.

The re-opening of state borders, very low levels of community transmission, and the rollout of the COVID-19 vaccine program has delivered a boost of optimism for investors, particularly sectors linked directly to the re-opening of the economy, in particular consumer discretionary, industrial and resources. However, companies that have been among the clear ‘winners’ from COVID-19 (e.g. Coles and JB Hi-Fi) will now have significantly higher comparable sales to meet or exceed in upcoming result periods to maintain their share price gains.

Looking back over the March quarter, returns were led by the telecommunications, financials and consumer discretionary sectors, with key companies producing stronger than expected results primarily driven by cost control and margin expansion. Notably, the banks reinstated larger dividend payouts and material writebacks of their COVID-19 related bad debt provisions, signaling to investors increased confidence in their earnings outlook. Long-term bond yields were up 77 basis points in response to stronger economic activity flowing through to the market, re-pricing higher inflation expectations. In this environment, banks should benefit with improved earnings growth.

Resources maintained their positive momentum with the global economic recovery continuing to gather pace. Miners including BHP (+9.6%) were driven by a resilient iron ore price and announcements of larger dividends at their recent February results. Energy sector Santos +14.2% and Oil Search +10.7% were also stronger performers as the Brent Crude price increased to US$64 per barrel.

Information Technology was the laggard sector, delivering around 10% in the March quarter, with several companies not matching their high expectations (e.g. Appen in the recent results period). Investors are pivoting away from COVID-beneficiary sectors like IT and Healthcare while shifting investor attention to cyclically exposed stocks and higher bond yields, which detract from the value of their long-term cash flows.

Source: Lonsec / Financial Express

The macroeconomic backdrop has not changed significantly over the March quarter and some key growth drivers have been strengthened. Australia is better positioned economically than most developed countries, the unemployment rate has not reached the peak that was initially expected, and fiscal and monetary stimulus is fueling an economic recovery, reflected in rising house prices. Terms of trade, especially rising commodity prices, have significantly boosted national income. Consumer sentiment is expected to remain resilient and wealth effects will encourage a normalisation in the savings rate, which should benefit consumer spending. Overall, stocks that are largely exposed to the economic cycle are expected to be well supported in this environment.

From a valuation perspective, the Australian equity market is trading on a one-year forward P/E ratio of nearly 19 times, which is circa 25% above the long-term average of 14.5 times and appears stretched relative to historical averages. The overall market appears to be moderately expensive and earnings growth needs to continue its upward trajectory over the next 12 months to support some of these elevated prices.

Issued by Lonsec Research Pty Ltd ABN 11 151 658 561 AFSL 421 445 (Lonsec). Warning: Past performance is not a reliable indicator of future performance. Any advice is General Advice without considering the objectives, financial situation and needs of any person. Before making a decision read the PDS and consider your financial circumstances or seek personal advice. Disclaimer: Lonsec gives no warranty of accuracy or completeness of information in this document, which is compiled from information from public and third-party sources. Opinions are reasonably held by Lonsec at compilation. Lonsec assumes no obligation to update this document after publication. Except for liability which can’t be excluded, Lonsec, its directors, officers, employees and agents disclaim all liability for any error, inaccuracy, misstatement or omission, or any loss suffered through relying on the document or any information. ©2021 Lonsec. All rights reserved. This report may also contain third party material that is subject to copyright. To the extent that copyright subsists in a third party it remains with the original owner and permission may be required to reuse the material. Any unauthorised reproduction of this information is prohibited.