While the use of a value approach or value (factor) bias is often associated with equity portfolios, the extraordinary events in early 2020 served as a reminder of the value bias inherent in many multi asset solutions. This bias results from the valuation factors inherent in both asset allocation and security selection decisions.

The emphasis managers place on ‘value’ in their asset allocation and security selection processes has impacted portfolio performance over the past several years given the headwinds ‘value’ as a factor has faced. Lonsec’s recent review of multi-asset funds emphasised the need for adequate risk management systems to ensure any ‘bets’ in the portfolio are intended and in line with managers’ strategic decisions. Moreover, Lonsec was interested to discuss the role of ‘value’ in asset allocation decisions alongside other factors including liquidity, sentiment and policy, and the timeframe in which managers frame their decisions.

In this thought piece Lonsec aims to answer why the last five years has been a challenge for asset allocators, the role the ‘value’ factor has played and why Lonsec believes it is vital that asset allocators and their investors understand the drivers and extent of any bias’s present in portfolios and the likely effect this will have on portfolio performance at different points in the cycle.

Asset allocation

Investment managers who build diversified portfolios of assets with allocations to an array of asset classes (i.e., multi asset portfolios) often use an asset allocation approach as the core building block of their portfolio construction process.

While there are numerous asset allocation approaches, the most recognised are long term ‘strategic asset allocation’ (SAA), medium term ‘dynamic asset allocation’ (DAA) and short term ‘tactical asset allocation’ (TAA). While some managers have defined their own asset allocation approach and associated acronym, their approaches invariably sit somewhere between long term SAA and short term TAA.

For managers who build portfolios based on a clearly defined asset allocation approach, capital market assumptions (i.e., forecasts for asset class returns, asset class risks and cross-asset correlations) are key inputs into the setting of portfolio asset allocation, regardless of the approach used.

When defining capital market assumptions for the forecast period, asset allocators commonly use expected returns, expected risk and correlations as the essential inputs into the asset allocation process. For SAA decisions, expected returns are heavily reliant on current valuations. DAA processes by contrast focus on medium term horizons of circa 18 months to 3 years and can focus on broader factors in determining the under and overweights to particular asset classes. In Lonsec’s experience, valuation will still play a role, and in some cases a heavy role, in determining positioning over these periods. For example, if equity markets are deemed to be trading at high valuations relative to long term averages (e.g., on metrics such as price to earnings multiples), asset allocators may choose to down-weight equities in their current asset allocation. This decision may be driven by the assumption valuation multiples will normalise in the ensuing period towards the long-term average (e.g., where a compression in earnings multiples drives a fall in share prices). Likewise, in the fixed income sphere, low yields and narrow spreads have meant allocating to these sectors has been a challenge. The difficulty with this approach is that valuations can overshoot for an extended period of time, especially when liquidity is higher than average and central bank policy has been supportive. The use of valuation metrics as inputs in asset allocation approaches is likely to create a bias towards asset classes offering attractive valuations and in turn creating value biases in multi asset portfolios.

The dominance of macro factors in overshadowing asset specific factors has continued to be a discussion point between Lonsec and multi-asset managers. Lonsec has found those using a framework to assess the economic and market cycle to have a more holistic DAA framework when compared to others using more simple methodologies.

Security selection

Alongside asset allocation, another dominant driver of positioning for multi asset managers is security selection. Having identified the desired portfolio asset class exposures, in order to select the securities for inclusion in each asset class managers will often analyse the prevailing valuation levels of securities or sectors. This analysis can involve drilling down to the sub asset class level, geographical location level, and the sector/industry level to find the best opportunities within an asset class.

While some managers may seek to build portfolios with diversified factor exposures, many managers tilt security selection away from seemingly expensive areas of securities markets and towards undervalued areas of securities markets.

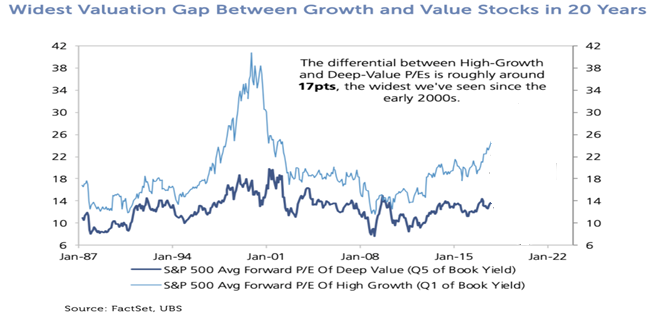

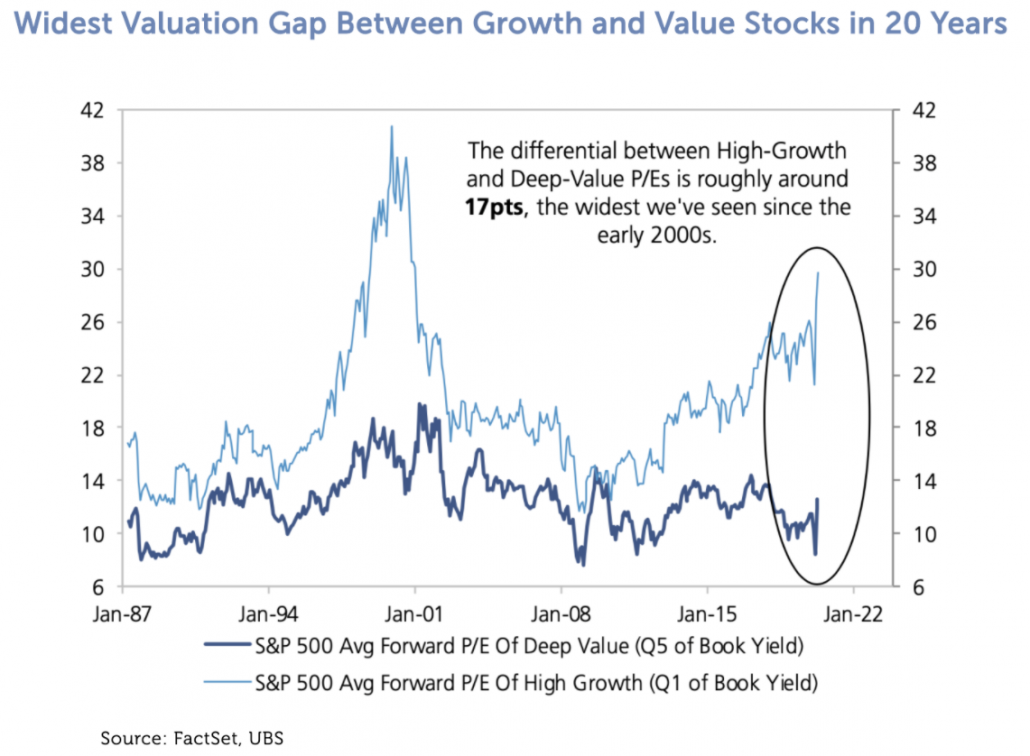

As Figure 1 shows, entering 2020 the valuation gap between growth equites and value equities had moved to highs not seen since the early 2000’s bubble:

Figure 1

While increasing exposure to cheaper areas of securities markets makes sense intuitively, where multi asset managers apply this approach across many of or all the underlying asset classes utilised, it may create a large value factor bias within portfolios. Lonsec believes managers need to be aware of these biases and ensure exposures are intended rather than unintended positions.

The last five years, and heading into 2020

In the years after the GFC, having taken official cash rates to record lows, the modus operandi of central banks has been to pump liquidity into economies and investment markets at any and every sign of trouble. This has helped to drive down bond yields and expected returns across all asset classes. The challenge of where to invest in this environment has been one impacting all asset allocators.

While managers have stuck to their investment and portfolio construction processes over this time, Lonsec notes there has been a disconnect between portfolio positioning and financial market performance. The challenge for managers over this period was to correctly form a view on the business cycle. With interest rates rising (albeit slowly) from late 2015 to 2018 and contrasting views on the emergence of inflation, there were divergent views on how portfolios should be positioned (over this period Lonsec has noted funds in its Variable Growth Assets > Real Return sector have been positioned at both ends of the risk spectrum). Likewise, views on the market cycle becoming later stage were predicated on valuations becoming more expensive across the board. Many of the managers we rate had been conservatively positioned due to this, and underperformed passive benchmarks which benefitted from the continued and increasing richness of valuations (particularly in geographies like the US, and sectors like Technology and Healthcare).

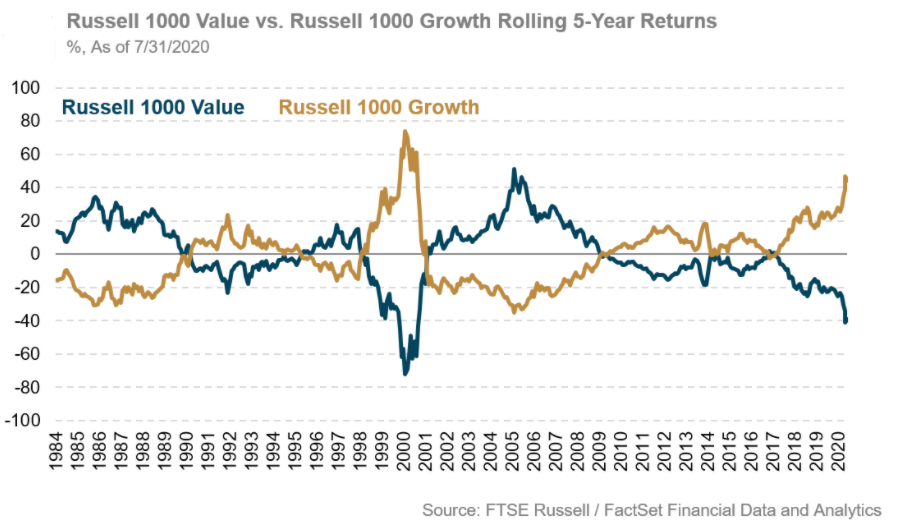

While there were signs of a pick-up in economic growth and a corresponding response from value and cyclical assets in late 2019 and some managers became more constructive on market outcomes, the three-year period leading into January 2020 undoubtably favoured strategies that invested in growth assets over value assets, as shown in Figure 2:

Figure 2

The 2020 experience – the bear market

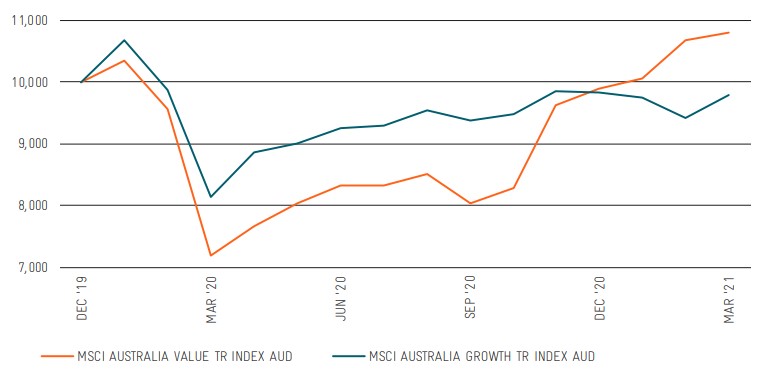

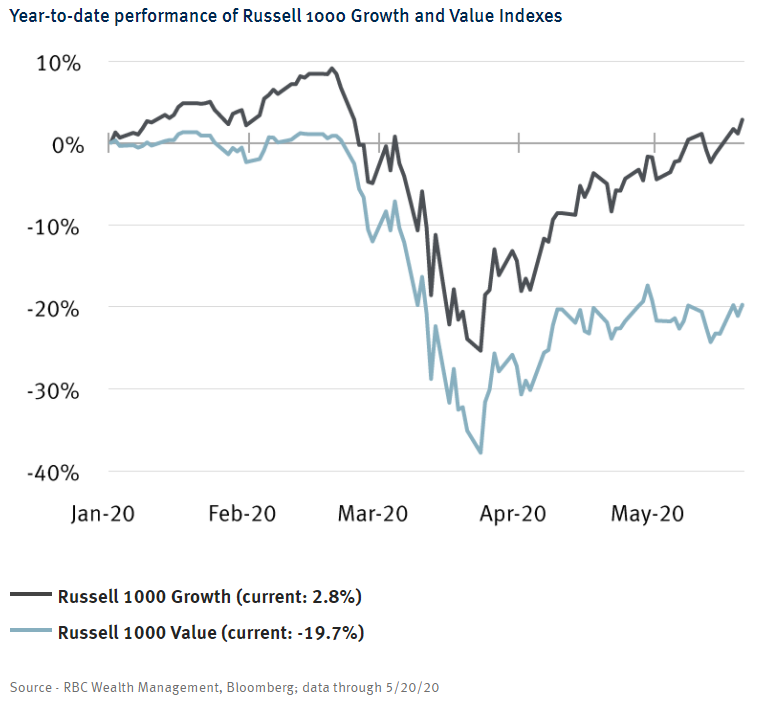

The COVID induced sell off that began in February 2020 saw value stocks fall faster and further than growth stocks through late March 2020. Value orientated strategies have at times underperformed at the beginning of equity bear markets, arguably as investors throw in the towel and finally pull the sell trigger on their worst performing stocks, and this was the case in 2020. Figure 3 shows that from 1 Jan 2020 to 20 May 2020, the performance of value stocks materially lagged that of growth stocks.

Figure 3

Figure 4 shows that the valuation gap between growth equities and value equites continued to reach new multi-year highs during and coming out of the COVID induced bear market:

Figure 4

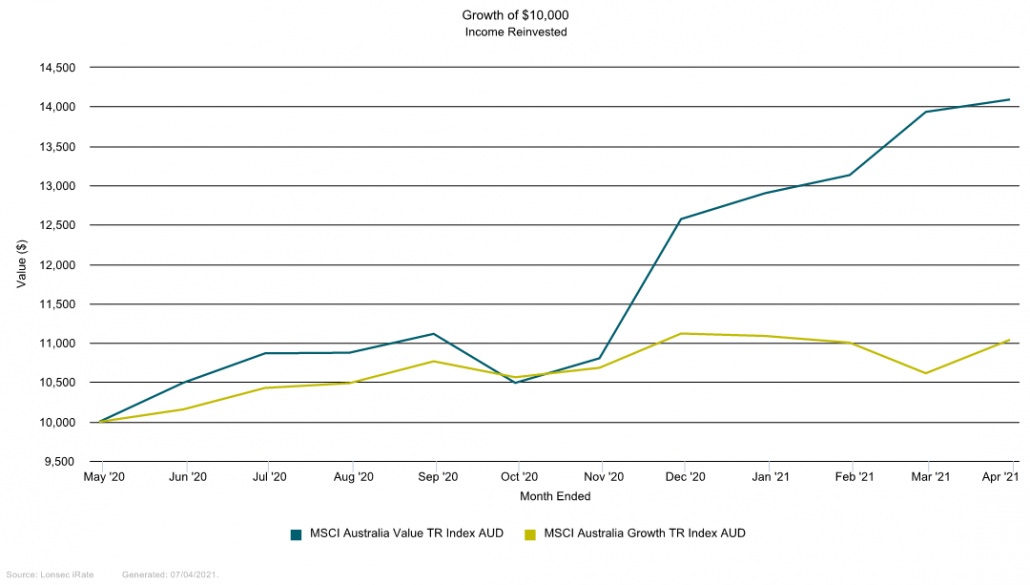

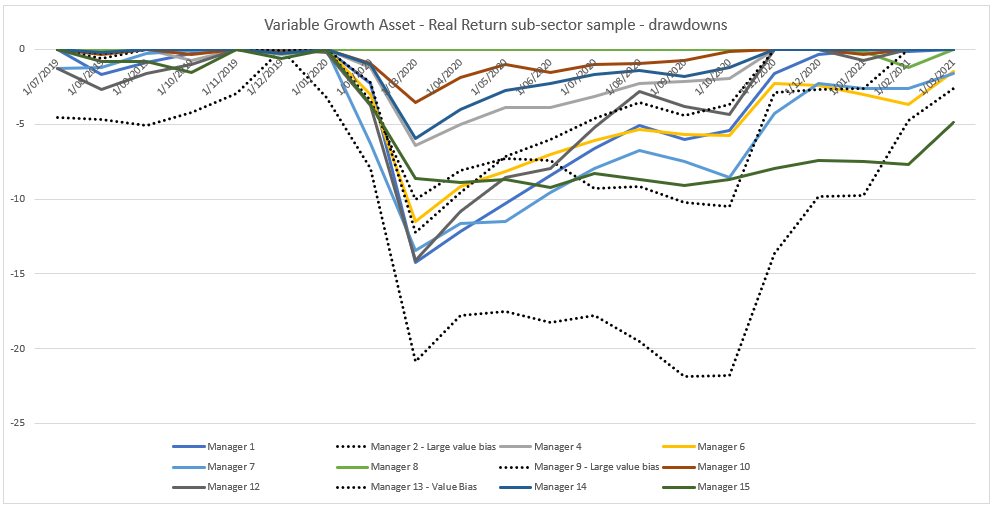

The 2020/21 experience (so far) – multi asset managers

The chart in Figure 5 shows the experience of a sample of managers in the Variable Growth Assets – Real Return sub-sector. While some multi asset managers suffered smaller drawdowns relative to peers by entering February 2020 defensively positioned based on valuations (and had been conservatively positioned for much of the prior two to three year period), other multi asset managers nimbly reduced risk exposures by reducing equity exposures or adding downside protection through derivatives.

Among the managers that suffered larger drawdowns relative to peers, many had pronounced value biases through their asset allocation and security selection approaches, in some cases adding significantly to cheap, cyclicals as the market sold off. These managers were impacted when growth styles started to recover more quickly. Lonsec notes, however, that those managers with value biases have bounced back (in some cases sharply) as the value rotation has taken hold since late 2020, though Lonsec notes it is too early to suggest how sustained this will be and may be somewhat dependent on the path of the economic recovery from here.

Lonsec believes articulation of the manager’s strategy to be important given it is likely to provide a greater understanding of how the manager and their fund is equipped to perform in different environments. Nonetheless, it is important to recognise that Lonsec’s ratings encompass a ‘through the cycle’ view on managers we assess.

Figure 5

Key takeaways

Whilst portfolios may be diversified at the asset class level, this may not be indicative of the inherent level of diversification overall within portfolios. As Lonsec has seen in its recent multi-asset review, biases towards the value factor have, in some cases, been high and exacerbated by biases coming from both asset allocation and security selection effects. Lonsec prefers to see diversification across not only style, but also strategy, geography, sector and factor. Value biases have been pronounced in some portfolios in recent years given high valuations and the belief in some quarters that the cycle was maturing. This positioning has proved a performance headwind against passively managed SAA weighted benchmarks in recent years and in recent months led to significant performance dispersion among different strategies.

Going forward, while it is difficult to time decisions over shorter periods, Lonsec expects greater levels of dispersion in markets which should provide greater opportunities for active asset allocators to extract alpha from markets. Lonsec continues to discuss the foundations for any active bets in portfolios and the framework behind such decisions. Moderately leaning into certain style or factor bets can be challenging but possible at points in the cycle when supported by a strong asset allocation framework.

When the value bias in an investment manager’s approach is compounded in the security selection process, Lonsec believes asset allocators must be cognisant of the degree of value bias in their portfolios to ensure this is in line with their strategy (or any factors for that matter). All bets must be intended with unexpected performance resulting for those unaware of their true exposures. As valuations have been shown to have stronger explanatory power on returns over longer term horizons, Lonsec also continues to progress conversations on the time horizon of manager’s decision making processes. Overall, Lonsec believes that asset allocators making shorter to medium term decisions should include value as one factor among others that may have increased forecasting power over the medium term.

Authors

Darrell Clark, Manager, Multi-Asset

Sebastian Lander, Senior Investment Analyst

Issued by Lonsec Research Pty Ltd ABN 11 151 658 561 AFSL 421 445 (Lonsec). Warning: Past performance is not a reliable indicator of future performance. Any advice is General Advice without considering the objectives, financial situation and needs of any person. Before making a decision read the PDS and consider your financial circumstances or seek personal advice. Disclaimer: Lonsec gives no warranty of accuracy or completeness of information in this document, which is compiled from information from public and third-party sources. Opinions are reasonably held by Lonsec at compilation. Lonsec assumes no obligation to update this document after publication. Except for liability which can’t be excluded, Lonsec, its directors, officers, employees and agents disclaim all liability for any error, inaccuracy, misstatement or omission, or any loss suffered through relying on the document or any information. ©2021 Lonsec. All rights reserved. This report may also contain third party material that is subject to copyright. To the extent that copyright subsists in a third party it remains with the original owner and permission may be required to reuse the material. Any unauthorised reproduction of this information is prohibited.