The coronavirus has had a major impact on equity markets in the past few days, and the uncertainty surrounding looks set to continue for some time. Peter Green, our Head of Listed Products, looks at the stocks that have been directly and indirectly affected, as well as some of the reporting season’s best and worst performers.

It has been a turbulent start to the year with Australia beginning the recovery process from the tragic bushfires followed by the threat of a global pandemic with cases of the coronavirus increasing across the globe. Despite these events markets did not flinch in January, with equity markets generating strong returns for the month as liquidity conditions continue to be supportive of markets.

If we look at previous incidents of viral outbreaks, such as SARS in 2003 and H1N1 (swine flu) in 2009, short-term corrections were within the range of 5% to 15%. These corrections were followed by strong rebounds. The consensus view is that global growth will be down in the first quarter of the year as a result of the coronavirus with the key variable being how long the threat of the virus persists.

While history is a useful guide in this case, it must be said that the effect of this epidemic is likely to be greater given China’s dominant presence in the global economy, given the faster spread of the disease and the measures taken to combat it. The extended closure of Chinese industry, restrictions on people movement, disrupted supply chains, declines in key commodity prices, bans on Chinese travel and the flow-on effect to confidence will severely hamper growth in China and the countries and regions most heavily reliant on China.

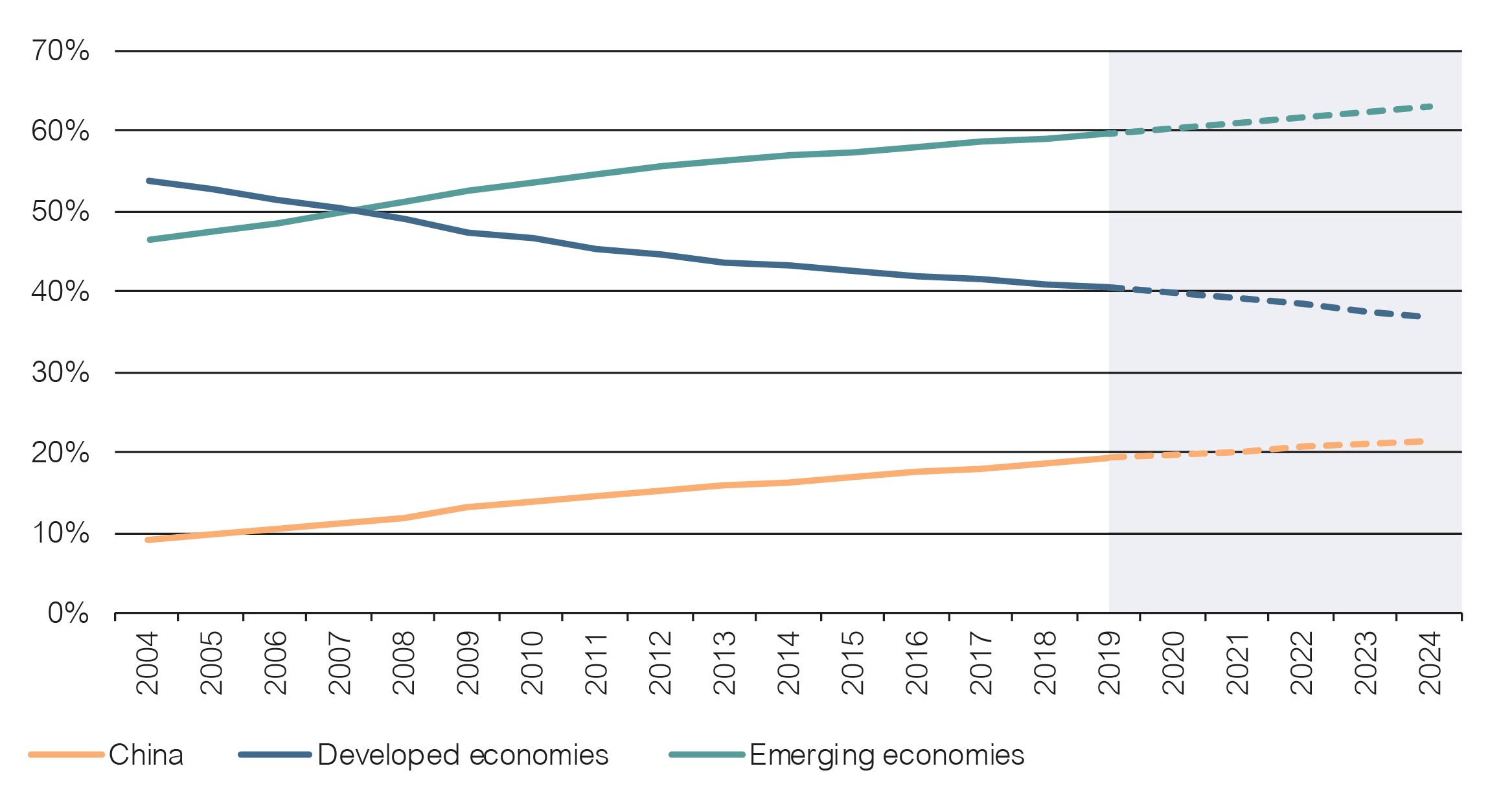

While at the time of the SARS outbreak China accounted for around 9.0% of global output on a PPP basis, it now accounts for 19%, and this proportion is only likely to increase in coming years, according to the IMF. China accounts for 18% of global tourism spending (up from 4.0% in 2008) while overall tourism (domestic and global) spending accounts for more than 10.0% of Chinese GDP and has been contributing almost 1.5% to annual GDP growth. To place China’s emergence on the global stage into perspective, in 2003 there were 20 million Chinese overseas visits and in 2018, 150 million. The Chinese economy accounted for about 30% of global growth in 2019. So a drop in Chinese GDP growth to 5.0% for the year, assuming the virus is contained within a short period, would detract 0.2–0.3% from global growth.

China now accounts for around 19% of global output

Source: IMF, Lonsec

From an Australian equities perspective, we are likely to see earnings outlook downgrades across a number of sectors, at a time of elevated valuations and a sub-par growth outlook. While earnings across the Healthcare, Consumer Staples and Infrastructure sectors should be relatively immune to recent events, based on Lonsec’s initial estimates, 2020 earnings estimates for the Resources (Energy, Iron Ore and Copper), Tourism/Travel and Consumer Discretionary sectors are likely to see significant one-off earnings revisions, capturing the impact of the coronavirus outbreak and the recent bushfires across Australia. However, such downgrades are unlikely to impact the long-term investment thesis for most companies and should be regarded as short-term headwinds, reflecting a series of one-off unfortunate events.

From an asset allocation perspective, Lonsec’s multi-asset portfolios remain very well diversified with only a small direct exposure to Chinese equity and bond markets. Consequently, our current focus is on the flow on effects that a sustained slowdown in Chinese growth may have on the domestic growth outlook given our close trading ties. As previously noted, our valuation indicators for Australian equities remain elevated, making them susceptible to a pullback should Chinese authorities’ attempts to stabilise growth fail. We have maintained our slight underweight positions in both global and Australian equities for the time being, however continue to monitor events closely.

While there is a high degree of uncertainty regarding the coronavirus outbreak, Lonsec notes that this event does pose a long “tail risk” for global markets should the outbreak get out of hand. These factors make it a challenging period for investors, where factors other than fundamentals are having a material impact on the trajectory of markets. In such an environment, we believe selective valuation opportunities will present themselves for long-term investors, however ensuring that your portfolio is diversified will be very important in navigating an increasingly volatile market environment.

Although the secrets of a long life remain a mystery, there are now over 300,000 centenarians across the globe and the numbers are rising. Most of us will not survive to 100 no matter how many green vegetables we eat, but there is no doubt life expectancy is increasing. In Japan, 2.5 times more adult than baby diapers are sold. Australian life expectancy from birth is among the highest in the world with the average man living to 80.7 and 84.9 for a woman. It assumes no improvement in healthcare which can increase life expectancy further.

The strength of equity markets during 2019 and the start of 2020 saw an increase in valuation premiums in the market resulting in a number of sectors trading at record highs. But the reporting season outlook has been impacted by a slowing global economy, the devastating bushfires across Australia and the coronavirus, elevating the risk profile of the market.

In this first video of our Reporting season series, Lonsec’s Listed Products Portfolio Manager, Danial Moradi, takes an in-depth look at how companies performed over the first two weeks of the reporting season.

Lonsec has partnered with AMP to make its Retirement Managed Portfolios available via MyNorth Managed Portfolio.

The portfolios harness the depth and breadth of Australia’s leading research provider, allowing users to build high-quality retirement solutions incorporating Lonsec’s best investment ideas. Underpinning the portfolios is Lonsec’s strict quality criteria, requiring funds to be rated ‘Recommended’ or higher by its investment research team.

“Our managed portfolios give financial advisers access to investment solutions supported by one of Australia’s largest investment research and consulting teams,” said Lonsec CEO Charlie Haynes.

“Being able to draw on our investment selection and portfolio construction expertise is a real plus, and we’re proud to be able to extend this access via the North platform users.”

Lonsec’s Retirement Managed Portfolios are objectives-based and focused on delivering an attractive and sustainable level of income while generating capital growth through a diversified portfolio of managed investments.

Lonsec offers three Retirement portfolios: Conservative, Balanced and Growth. Each are designed to achieve different risk and investment objectives over various timeframes. They are constructed using a range of funds that play a specific role, such as income generation, capital growth and risk control, and backed by Lonsec’s rigorous governance and review processes.

“Our Retirement Managed Portfolios have been constructed to manage the risks most relevant to investors in the retirement phase,” said Lonsec’s Chief Investment Officer Lukasz de Pourbaix.

“By diversifying across asset classes, managers and return sources, we aim to manage risks such as capital drawdown, which can materially impact the longevity of a retirement portfolio, particularly in the early stages of transitioning from superannuation to the pension phase of investing.”

“We’re very excited to be working with AMP to make these portfolios available to AMP’s North wrap users.”

Inclusion on North further expands the distribution of Lonsec’s Managed Account offering, following its existing availability on the BT, Macquarie, HUB24, Netwealth and Praemium platforms.

Lonsec’s retirement portfolios have been constructed to meet the income and capital objectives of investors in the retirement phase as well as to manage risks that are specifically relevant to retirees.

AMP’s North platform offers advisers flexible and efficient access to a range of investment products, which now include Lonsec’s retirement portfolios, giving advisers the tools they need to meet their clients’ goals.

The FASEA Code of Ethics Standard is now in force as of 1 January 2020, and the challenge for advisers is not just to pass the exam but also to make the necessary changes to their business practices.

According to leading research house Lonsec, the Code now requires advisers to demonstrate that they are acting in their client’s best interest while avoiding even a ‘perception’ of conflicted recommendations.

“For advisers the FASEA standards are no longer an intellectual exercise. Despite the practicality issues, they are now the yardstick against which they will be judged by regulators, clients and the community,” said Lonsec CEO Charlie Haynes.

“The reality is that the only way an adviser can comply with the standards effectively and efficiently is to access quality investment research and technology tools that enable them to provide detailed product comparisons across all asset classes, including superannuation funds and investment options.

“This goes to the heart of Standard 9 of the Code of Ethics, which requires advisers to make recommendations with competence.”

Lonsec also foreshadowed that conflicted remuneration, even if an adviser considers it to be minor, manageable, or largely irrelevant, could put licensees in breach of the standards.

Standard 3 of the FASEA Guidelines states that an adviser is in breach “if a disinterested person, in possession of all the facts, might reasonably conclude that the form of variable income could induce an adviser to act in a manner inconsistent with the best interests of the client.”

This means that all conflicts, even a preference to use an in-house practice or dealer group product, could be viewed as an inducement to act in a way that isn’t in the client’s best interest.

“Avoiding even perceived conflicts is now a requirement for advisers, so practices should strongly consider moving to a conflict-free environment to safeguard their position,” said Mr Haynes.

“Lonsec is now offering to solve this and help advisers moving forward by acquiring the investment management rights from existing portfolios and to manage the investment process on behalf of the adviser without ongoing conflict.”

Standard 6 also raises the bar for advisers, stating: “Where your clients indicate they only wish to invest in ethical or responsible investments, you will need to consider whether limiting your product recommendations in this manner is appropriate.”

According to Lonsec, meeting this standard means going beyond recommending branded ‘ethical’ products to understanding exactly what the product invests in and whether this indeed aligns with the client’s expectations.

“Advisers now have a legal responsibility to ensure their client’s preferences are taken into account,” said Mr Haynes. “For example, if the client doesn’t want fossil fuels in their portfolio, simply recommending an ESG product probably won’t be sufficient from now on. The adviser needs to have a complete understanding of the product’s underlying investments and its process.

“That’s why Lonsec is introducing a new sustainability rating and will provide data on how individual investment products stack up against the United Nation’s 17 Sustainable Development Goals. We want to give advisers all the tools and information they need to deliver advice that they can clearly demonstrate meets the FASEA standards and their best interest duty.”

According to estimates from leading research house SuperRatings, super funds had a positive start to 2020, with the median balanced option returning 1.9% in January, driven predominately by gains from Australian and International shares.

The start of February was a different story as markets were affected by the outbreak of the Coronavirus, which led to a selloff in global share markets as investors sought out safe-haven assets.

Asian equity markets have borne the brunt of the initial impact, but the effects are likely to be felt across global markets, noting that previous outbreaks over the last two decades have resulted in short–term equity market corrections within a range of 5–15%.

As super funds face the new normal of lower returns and yields, managing volatility is becoming increasingly necessary. However, despite the current swings in the market, SuperRatings said funds remained focused on long-term member outcomes.

“The funds we’ve spoken to are not responding to the current market situation with knee-jerk reactions,” said SuperRatings Executive Director Kirby Rappell.

“They’re watching developments closely, but so far market volatility has been in line with similar risk events experienced in recent years. Fund investment strategies are generally well placed to manage these types of movements.”

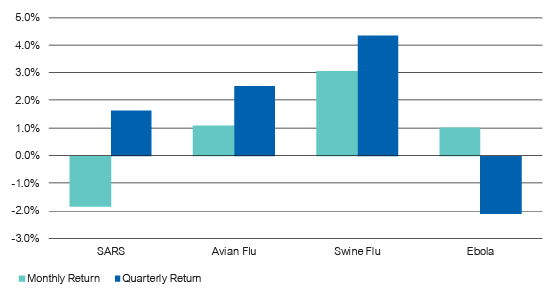

Looking back at previous epidemics, such as the Ebola outbreak in 2018 or the SARS epidemic back in 2003, Australian super funds have proved relatively resilient to short-term market movements. Quarterly returns during each episode have ranged between -2.1% and +4.3%, with markets largely unfazed over longer periods.

Outbreaks and SR50 Balanced Index performance

Source: SuperRatings, Financial Express

Whether the effect of the Coronavirus has a more lasting impact on markets remains to be seen, but funds are unlikely to implement any dramatic changes to their investment strategies without further evidence that the virus will deal more prolonged damage to the global economy.

Con Michalakis, Chief Investment Officer at StateWide Super, said that while there would undoubtedly be some economic fallout, the fund remains focused on long-term member outcomes. “This is a classic case of a black swan, and like all black swans the markets struggle with uncertainty,” said Mr Michalakis.

“What we can be sure about is that the economy in China and Australia will be slower due to the restrictions in place in the first quarter of 2020. However, from a long-term perspective, diversification and strategy based on member age and risk tolerance is more important.”

Suzanne Branton, Chief Investment Officer at CareSuper, said the fund’s investment strategies are designed to provide downside protection during bouts of market turmoil.

“When new influences on the investment outlook emerge, it’s important to analyse and monitor these closely,” said Ms Branton.

“There could be a short-term impact that provides investment opportunities or avenues to adjust positioning. However, there are reasons to expect a more short-term rather than extended large-scale market impact. Our investment approach is structured to deliver downside protection so our investment program resilience to short-term volatility is high.”

Super funds post solid returns in January as share markets powered into 2020

Super funds started the year in positive territory as momentum in local and international share markets carried through into the new year. This was quickly reversed following the outbreak of the Coronavirus and the ensuing drawdown in markets, but over longer periods super fund returns are holding up remarkably well.

Over 12 months to the end of January, the median balanced option returned an estimated 13.8%, while the median growth option return was estimated at an impressive 16.2%. Returns over the past seven years are estimated at 8.8% and 9.8% respectively.

Estimated accumulation returns (% p.a. to end of January 2020)

| 1 yr | 3 yrs | 5 yrs | 7 yrs | 10 yrs | |

| SR50 Growth (77-90) Index | 16.2% | 10.2% | 8.2% | 9.8% | 8.8% |

| SR50 Balanced (60-76) Index | 13.8% | 9.1% | 7.7% | 8.8% | 8.2% |

| SR50 Capital Stable (20-40) Index | 7.7% | 5.3% | 4.6% | 5.3% | 5.6% |

Source: SuperRatings

Pensions have delivered even higher returns than accumulation products, with the median balanced pension option returning an estimated 15.4% over the 12 months to the end of January, while the median growth pension option had an estimated return of 18.0%. Over the past seven years each have returned 9.6% and 10.8% respectively.

Estimated pension returns (% p.a. to end of January 2020)

| 1 yr | 3 yrs | 5 yrs | 7 yrs | 10 yrs | |

| SRP50 Growth (77-90) Index | 18.0% | 11.4% | 9.3% | 10.8% | 9.7% |

| SRP50 Balanced (60-76) Index | 15.4% | 9.8% | 8.1% | 9.6% | 9.0% |

| SRP50 Capital Stable (20-40) Index | 8.9% | 6.2% | 5.2% | 5.9% | 6.3% |

Source: SuperRatings

“We expect to see volatility appear more frequently over the course of 2020, but overall our outlook for super funds is positive,” said Mr Rappell.

“Long-term returns will continue to hold up despite the challenging return environment we find ourselves in at present. Members should look forward to a solid 2020, but expect some bumpiness along the way.”

The outbreak of the coronavirus in over 28 countries has sent shockwaves through global financial markets over the past fortnight with increasing levels of uncertainty and misinformation evident across a number of regions. While there are many unknowns regarding this outbreak, there is likely to be continued disruption to economic activity ahead, which is unlikely to subside until the outbreak is brought under control.

The impact of the coronavirus on equity markets is likely to be multi-faceted with the potential to impact earnings across a numbers of sectors over 2020. While Asian equity markets are likely to take the brunt of the initial impact, the effects are likely to be felt across global markets, noting that previous outbreaks over the last two decades have resulted in short–term equity market corrections within a range of 5-15%.

Implications on the Australian equity market

From an Australian equities perspective, we are likely to see earnings outlook downgrades across a number of sectors, at a time of elevated valuations and a sub-par growth outlook, particularly as we head into the February reporting season. While earnings across the Healthcare, Consumer Staples and Infrastructure sectors should be relatively immune to recent events, based on Lonsec’s initial estimates, 2020 earnings estimates for the Resources (Energy, Iron Ore and Copper), Tourism/Travel and Consumer Discretionary sectors are likely to see significant one-off earnings revisions, capturing the impact of the coronavirus outbreak and the recent bushfires across Australia. However, such downgrades are unlikely to impact the long-term investment thesis for most companies and should be regarded as short-term headwinds, reflecting a series of one-off unfortunate events.

Lonsec’s asset allocation views

From an asset allocation perspective, Lonsec’s multi-asset portfolios remain very well diversified with only a small direct exposure to Chinese equity and bond markets. Consequently, our current focus is on the flow on effects that a sustained slowdown in Chinese growth may have on the domestic growth outlook given our close trading ties. As previously noted, our valuation indicators for Australian equities remain elevated, making them susceptible to a pullback should Chinese authorities’ attempts to stabilise growth fail. We have maintained our slight underweight positions in both global and Australian equities for the time being, however continue to monitor events closely.

While there is a high degree of uncertainty regarding the coronavirus outbreak, Lonsec notes that this event does pose a long “tail risk” for global markets should the outbreak get out of hand. These factors make it a challenging period for investors, where factors other than fundamentals are having a material impact on the trajectory of markets. In such an environment, we believe selective valuation opportunities will present themselves for long-term investors, however ensuring that your portfolio is diversified will be very important in navigating an increasingly volatile market environment.

The Australian Health Care sector has had another stellar year, with the S&P/ASX 200 Health Care Index providing a substantial 43.5% total return over 2019. This was substantially higher than the still impressive 23.4% return provided by the broader S&P/ASX 200 Index. These strong health care returns were largely due to impressive earnings growth being recorded by some larger names such as CSL Limited (CSL) and Resmed Inc (RMD), up 50.8% and 39.3%, respectively. In addition, recent interest rate cuts globally in the face of a more challenging economic outlook has added fuel to the rally as health care is seen as having structural growth drivers that have a lower correlation to the economic cycle.

However, consistent with such a strong rally in share prices, valuations in the sector now appear full versus longer-term trends. This confluence of strong earnings performance with full valuations should provide investors with a reason to pause and assess the risk-adjusted returns available to them going forward. But to do so, it is critical that investors develop a deeper understanding of the bottom-up fundamentals of the health care companies themselves. While the outbreak of the Coronavirus is unlikely to have a direct effect on Australia’s health care names, a risk-off environment could see investors attracted to the defensive characteristics of the sector.

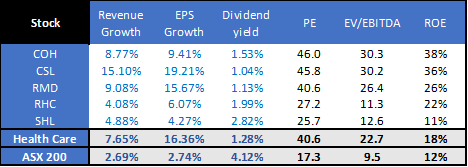

A review of consensus estimates on a 12-month forward basis quickly establishes that the market is firmly of the belief that the fundamentals for the Health Care sector remain robust. Current consensus estimates are for top-line sales growth of 7.7% and even stronger earnings growth of 16.4% due to the operating leverage inherent in these companies. These top and bottom-line estimates are well ahead of the broader market, with the S&P/ASX 200 Index consensus estimates being for both top-line growth and earnings growth of around 2.7%.

However, this above trend growth comes with a hefty price tag. The forward price-to-earnings (PE) ratio for the S&P/ASX 200 Health Care Index is 40.6x, well above the 17.3x for the S&P/ASX 200 Index. In fact, by our estimates the current PE ratios for both CSL and RMD are currently two standard deviations above their 10-year harmonic means, and Cochlear Limited (COH) is one standard deviation above. This is also reflected in the current dividend yield projections, with the consensus yield (pre-franking) being a meagre 1.4%, again well below the market yield of 4.3%.

Then again, with the sector return on equity (ROE) projections being a healthy 18%, there’s a strong argument that health care investors are well served by boards reinvesting capital rather than paying it out as a dividend.

Health Care Sector 1-Year Forward Outlook

Source: Thomson Reuters, Lonsec Research

The Australian Health Care sector is dominated by CSL, with its market cap of around $128 billion, making up over 60% of the Health Care Index’s $208 billion capitalisation. This concentration in CSL only grew stronger over 2019 as its performance outpaced most of its peers. CSL has benefitted from strong global demand for its plasma products, especially in the US and increasingly in China. CSL is benefiting from an ageing population, increased development and spending on rarer diseases, and a unique ability to source their own raw material ‘plasma’ via an array of collection centres throughout the US.

This has been complemented by the acquisition of flu vaccination supplier Sequirus, which CSL has transformed from a loss-maker into a business with an expected EBIT of $200 million in FY20. Given this backdrop, CSL is likely to continue to benefit from a prolonged earnings upgrade cycle as seen by its sector leading EPS consensus growth target of 19.2% for FY21. Investors, however, will be required to pay up for it with a forward PE of 46x.

The broader Health Care sector is rounded out by a range of large-to-mid-cap medical device and medical service companies as well as an emerging tail of bio-tech companies which have strong runways for growth but are at an earlier stage of their development. Medical device companies such as COH and RMD have enjoyed earnings upgrade cycles, benefiting from strong investment in R&D and increased market penetration.

These factors are expected to continue, with consensus estimates being for EPS growth of 10–20%. This compares to the medical service providers such as Ramsay Health Care Limited (RHC) and Sonic Healthcare Limited (SHL), which have more subdued growth expectations (4–6%) due to regulatory and consumer preference risks. Nonetheless, these providers are still expected to be long-term beneficiaries of an aging population. Despite this slightly different earnings profile, both these sub-sectors are trading on a forward PE well above the market. However, due to the relatively stronger EPS trajectory, the medical device entities are trading at much higher multiples which are more commensurate with CSL.

The Australian Health Care sector has provided investors with very strong investment returns over the last year driven largely by earnings growth above the broader market due to positive structural tailwinds. The Australian segment is also demarcated by companies such as CSL which have strong corporate cultures which emphasise product innovation and operational excellence, factors which continue to provide them with a competitive edge globally. However, the strong earnings upgrade cycle in a ‘low growth’ world has seen very strong investor interest leading to valuations being stretched. Also, the sector is not homogenous with sub-sectors having different earnings profiles and risks. This mix of strong fundamentals with stretched valuations will continue to make an investment in Health care stocks more suited for investors with longer investment horizons.

Happy New Year and welcome back! It has been a tumultuous time for our country and our thoughts go out to those that have lost homes and loved ones due to the bushfires that have engulfed Australia.

Calendar year 2019 saw most asset classes generate very strong returns with many delivering double-digits returns. Australian equities, as measured by the S&P/ASX 300 Index, returned 23.8%, while global equities, as measured by the MSCI World ex Australia Index AUD, returned 27.6% for the year. At the other end of the asset classes spectrum, bonds also posted strong returns with Australian bonds, as measured by the Bloomberg AusBond Composite 0+ Year Index AUD, returning a solid 7.3% for the year. These returns were generated despite concerns over US-China trade tensions, Brexit, arguably high asset prices and mixed economic news.

A key factor contributing to this market strength has been the fact that interest rates appear to be on hold in the US and possibly heading lower in Australia. This is making investing in growth and interest rate sensitive assets, such as property and infrastructure, attractive when compared to holding your money in cash. Additionally, some of the economic indicators that were trending down, such as the PMI (Purchasing Manager’s Index), seem to have stabilised and the consumer seems to be holding up.

In 2020 we are paying particular attention to three key themes:

- Valuations

Asset classes are generally trading at fair to expensive territory with US equities appearing the most expensive based on most valuation measures. While interest rates are low these valuations may be sustainable in the near term. However, we expect that at some point valuations will come back into vogue. Timing turning points is difficult however on a forward-looking basis our expectation would be that ‘expensive’ asset classes will generate lower returns in the future. Based on this we retain our slightly underweight exposure to equity markets heading into 2020 favoring real assets and alternative assets. - The cycle

Much has been written about being late cycle and we think that we are at the later stages of the cycle. There are signs that some economic indicators have stabilised, which markets view favorably. Key things to watch in 2020 will be the consumer and household savings rate, which has been rising, and the possible flow on effect on consumption. - X-factors

Despite strong market returns, 2019 saw bouts of volatility caused by geopolitical issues including the US-China trade tensions. We expect this geopolitical environment to continue in 2020. Furthermore, we have seen geopolitical tensions rise in the Middle East with growing concerns over US-Iran relations. Such events create market uncertainty and market volatility in the short-term.

We wish everyone a prosperous and safe 2020.

Important information: Any express or implied rating or advice is limited to general advice, it doesn’t consider any personal needs, goals or objectives. Before making any decision about financial products, consider whether it is personally appropriate for you in light of your personal circumstances. Obtain and consider the Product Disclosure Statement for each financial product and seek professional personal advice before making any decisions regarding a financial product.