It sounds simple enough: invest in things that are good for the planet and society. Investing sustainably should be that simple, but in practice things are a lot less straightforward.

Confusion quickly sets in when we try to navigate the different approaches to sustainable investing. Much of this confusion stems from the plethora of industry terminology and definitions, and a general lack of understanding about how different product issuers approach questions around sustainability. Advisers with clients serious about taking an ethical and sustainable approach to their investment decisions are often left to un-muddy the waters.

Sustainable investing is a simple concept, but it’s not always simple to implement. The following three steps will help you clarify the sustainability issue and find an investment solution that genuinely meets your needs and expectations.

1. Understand the product issuer’s frame of reference

Not everyone thinks of sustainability in the same way. Some may think of it as actively avoiding certain industries, while others may see it as a way of mitigating the risk of out-dated industrial processes, bad PR, or the threat of disruption.

This can lead to a number of misunderstandings that can be detrimental to your objectives. Before we begin comparing different sustainable investment offerings, it’s necessary to nail down some terms:

ESG (environmental, social and governance) investing: The ESG approach to investing involves taking into account ESG factors (i.e. impact on climate change, board composition, or relations with employees, suppliers and the community) as they relate to a particular business, using a systematic research process. ESG factors are used to enhance traditional financial analysis by assessing the risk these factors pose to a company’s business model and using this information to optimise their portfolio.

Impact investing: The aim of impact of investing is to make a positive difference by investing specifically in businesses, non-profits or other organisations that are seeking to improve the world through the development of new technologies (e.g. clean energy or sustainable agricultural practices), the provision of essential community services (e.g. open banking, micro-finance, medical services), or the construction of critical infrastructure. The bulk of impact investing is done at scale by institutional investors and major philanthropic organisations.

Sustainable investing: The sustainable investing approach specifically targets sustainable themes (e.g. low carbon industries, Paris or UN SDG-aligned outcomes) and avoids certain harmful businesses and industries (e.g. tobacco, fossil fuels, gambling, weapons manufacturing). Sustainable investing may incorporate elements of ESG and even impact investing, but with the goal of achieving investment goals while considering the activities and practices of the underlying companies in the portfolio.

Each of these types of investing fall under the broader rubric of ‘Responsible Investment’ (RI). While these definitions are similar, they also differ in some important ways. For example, ESG, in contrast to sustainable investing, tends to be more focused on process than outcomes. While investment decisions may be informed by a sustainable overlay, an ESG fund manager may invest in unsustainable companies if it makes sense from a risk and return perspective.

ESG is a perfectly valid process, but it is important to understand the framework used by individual fund managers and how it aligns with your own values and expectations.

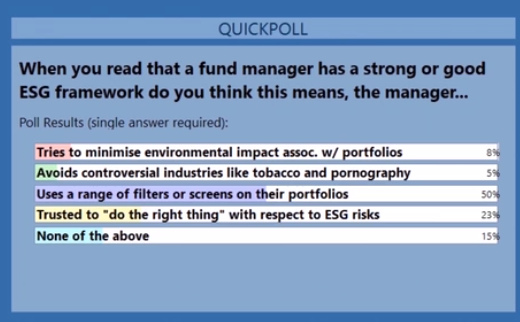

In Lonsec’s experience, ESG is interpreted and implemented in different ways. A survey of Lonsec’s financial advisers revealed a wide variety of responses when it comes to defining ESG. Half of advisers surveyed believed that a strong ESG framework means using a range of filters or screens on the portfolio. While this might seem like a reasonable assumption, for most fund managers, what really defines an ESG product is simply whether ESG risks are considered when making investment decisions. It doesn’t speak to the actual outcome, i.e. the companies and activities the product invests in.

Lonsec’s adviser survey revealed some confusion about the meaning of ESG

Source: Lonsec

This highlights the importance of digging deeper to find out what the product issuer means when they label a product ‘responsible’, ‘ethical’, ‘ESG’, or ‘sustainable’. It might not mean what you think it means, and it may be something different from what your client is looking for.

2. Determine what your client’s expectations are

We all have different values, priorities, and objectives. When we aim to invest sustainably, we will naturally be forced to make trade-offs. Investing in financial markets means accepting that we’ll end up with some exposure to things we don’t like. Even a company with impeccable green credentials will leave some carbon footprint. And environmental considerations may be only part of the equation. Some companies might be investing in green energy but still be lagging on gender equality and other social indicators. There is no perfect company, and likewise no perfect portfolio.

This is where individual, subjective values come into play. It’s up to the adviser to work with the client to determine their investment objectives—including risk and return preferences—while thinking about the types of exposures they are comfortable with from a sustainability perspective.

For this reason, not all self-described ESG or sustainable investment products will suit. For example, an ESG product may still invest in industries like tobacco and coal if it makes sense from a pure risk and return perspective. While this would suit some investors, it would not be appropriate for someone who is looking specifically to avoid investing in these industries.

When Lonsec assesses an investment product’s sustainability, it considers both sustainability and ESG. We seek to understand the effectiveness of the fund manager’s ESG process, but ultimately we’re interested in the product’s underlying portfolio: the companies, industries, and activities the product invests in.

If your clients are serious about investing sustainably, you should have a full discussion about exactly what it is they’re looking for so you know which products can best meet their needs. As regulations and standards become more stringent, we also need to be more cognisant of our obligations. The FASEA Code of Ethics Standard requires advisers to act in the best interests of their clients, which means product recommendations must be appropriate to meet the client’s objectives while considering their broader, long-term interests. This includes any social or ethical preferences the client might have.

The Financial Planning Association (FPA) guidelines on the FASEA Code of Ethics states: “Financial advisers should ask their clients if there are any environmental, social or ethical considerations that are important to them”. This involves having the sustainability conversation, determining the approach that works for you as the client, and recommending a solution that meets your needs and expectations.

3. Cut through the piles of data

Once you’ve established what the client is looking for, the next step is to identify suitable investments that fit our criteria. If you’ve picked up an ESG research report lately, you’ll know these tend to be stuffed full of metrics, some of which may not even be directly relevant to us. It’s difficult to know who these reports are designed for, because most investors and many advisers would suffer a severe bout of MEGO (‘my eyes glaze over’) if they tried to read through it.

Data is central to sustainable investing. Without the right data—and without the right quality of data—we can’t make good investment decisions. But the key is bringing this data together in a way that’s clear and actionable. A data dump is next to useless, even if the data itself is perfectly good.

Effective sustainability research is able to look through an investment product’s portfolio to assess sustainability at the security level, taking account of each company’s production methods, their role in the supply chain, and any second- and even third-order effects resulting from their activities. It also needs to summarise this in a digestible format that can be read and understood by advice clients, providing a clear rationale for why the product was recommended for them.

As an example, Lonsec’s sustainability reports are only two pages long, but they bring together a vast array of data to enable better decision making. The reports show the product’s exposure to and alignment with the United Nation’s 17 Sustainability Development Goals (SGDs), as well as ten controversial industries like fossil fuels, gambling, and tobacco. The product’s overall sustainability is presented in a single Sustainability Score, measured between one and five bees (a widely recognised symbol of sustainability given the critical role they play in our ecosystem).

Good sustainability research goes beyond product labels to tell clients exactly what they are investing in. It should also make it easier for you as the adviser to demonstrate the value of your advice and recommendations in a tangible way, without a deluge of extraneous metrics that confuse your message and make it harder for investors to understand the real benefit of your investment solution.

Keep communicating the benefits

Regular communication is the key to client retention. We all know this, but in reality maintaining both the frequency and relevance of our communications can divert us from other necessary business operations, including winning new clients and growing our advice practice. Having a suite of managed portfolios can help scale not only your investment process but also your portfolio communications, making the task of portfolio reporting and the generation of individual client communications significantly easier.

Once we have the right investment solution in place, we need to be proactive in communicating the benefits. Again, the right research and reporting is crucial. The sustainability conversation doesn’t end once the client’s portfolio is place. It will need to evolve over time, just as community expectations and client preferences change. But if we can do this successfully, we can create even more value for our clients, and add a whole other dimension to the value of our advice offering.

IMPORTANT NOTICE: This document is published by Lonsec Investment Solutions Pty Ltd ACN 608 837 583, a Corporate Authorised Representative (CAR 1236821) (LIS) of Lonsec Research Pty Ltd ABN 11 151 658 561 AFSL 421 445 (Lonsec Research). LIS creates the model portfolios it distributes using the investment research provided by Lonsec Research but LIS has not had any involvement in the investment research process for Lonsec Research. LIS and Lonsec Research are owned by Lonsec Holdings Pty Ltd ACN 151 235 406. Please read the following before making any investment decision about any financial product mentioned in this document.

DISCLOSURE AT THE DATE OF PUBLICATION: Lonsec Research receives a fee from the relevant fund manager or product issuer(s) for researching financial products (using objective criteria) which may be referred to in this document. Lonsec Research may also receive a fee from the fund manager or product issuer(s) for subscribing to research content and other Lonsec Research services. LIS receives a fee for providing the model portfolios to financial services organisations and professionals. LIS’ and Lonsec Research’s fees are not linked to the financial product rating(s) outcome or the inclusion of the financial product(s) in model portfolios. LIS and Lonsec Research and their representatives and/or their associates may hold any financial product(s) referred to in this document, but details of these holdings are not known to the Lonsec Research analyst(s).

WARNINGS: Past performance is not a reliable indicator of future performance. Any express or implied rating or advice presented in this document is limited to general advice and based solely on consideration of the investment merits of the financial product(s) alone, without taking into account the investment objectives, financial situation and particular needs (“financial circumstances”) of any particular person. Before making an investment decision based on the rating or advice, the reader must consider whether it is personally appropriate in light of his or her financial circumstances or should seek independent financial advice on its appropriateness. If the financial advice relates to the acquisition or possible acquisition of a particular financial product, the reader should obtain and consider the Investment Statement or the Product Disclosure Statement for each financial product before making any decision about whether to acquire the financial product.

DISCLAIMER: No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented in this document, which is drawn from public information not verified by LIS. The information contained in this document is current as at the date of publication. Financial conclusions, ratings and advice are reasonably held at the time of publication but subject to change without notice. LIS assumes no obligation to update this document following publication. Except for any liability which cannot be excluded, LIS and Lonsec Research, their directors, officers, employees and agents disclaim all liability for any error or inaccuracy in, misstatement or omission from, this document or any loss or damage suffered by the reader or any other person as a consequence of relying upon it.

Copyright © 2021 Lonsec Investment Solutions Pty Ltd ACN 608 837 583 (LIS). This document may also contain third party supplied material that is subject to copyright. The same restrictions that apply to LIS copyrighted material, apply to such third-party content.