Global equity markets in 2020 had a promising start to the year as the S&P 500 Index reached a new record peak of 3,380 on 20 February 2020, backed by better macroeconomic data and the prospect of reduced geopolitical headwinds (particularly on the US-China trade front).

However, the progressive realisation across financial markets that COVID-19 represented an existential threat to society necessitating the shutdown of whole swathes of the economy triggered a sharp sell down in mid to late March, sending the S&P 500 index falling by 34% to a low of 2,237 on 23 March 2020. The US equities market tripped circuit breakers four times in two weeks (March 9, 12, 16 and 18). The circuit breakers pause trading for 15 minutes in the event of a sudden 7% fall.

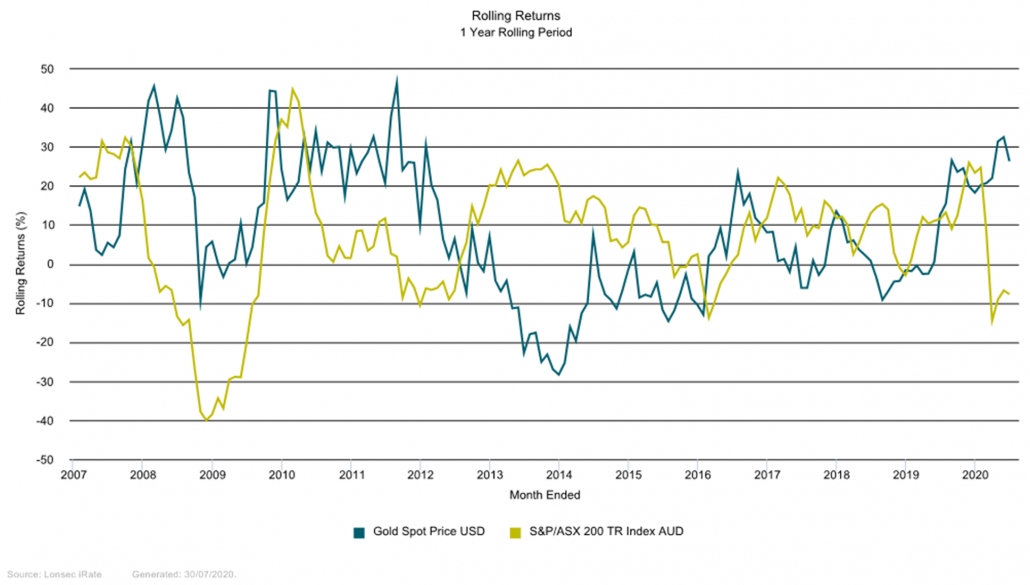

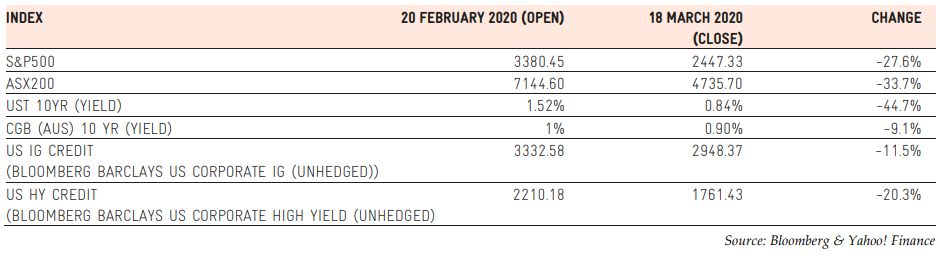

Key indices were hit hard as the coronavirus spread globally

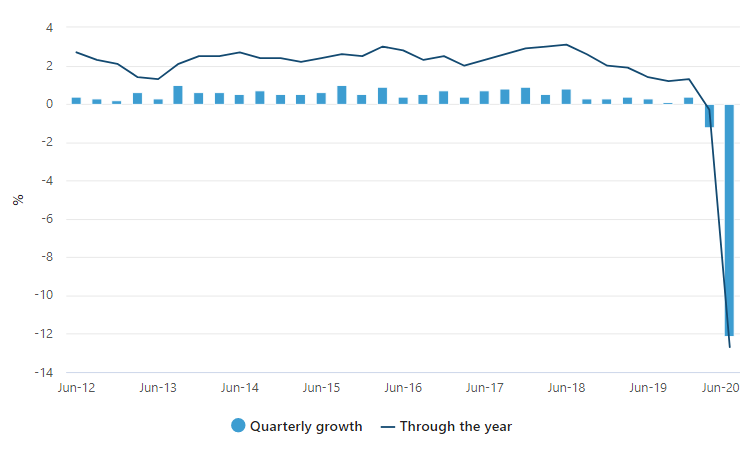

Assets with any risk were sold off. Equities expectedly suffered steep drawdowns with the US and Australia, for instance, entering bear markets. This also marked the close of the longest bull market in US history which lasted some 11 years. Credit also suffered heavy losses with high yield nursing a drop of some 20%. US Treasuries retained their safe harbour status with yields collapsing by nearly 30%. The same cannot be said about Australia’s government bonds which experienced rising yields and casting a cloud over fixed income portfolios.

The sell-off was exacerbated by an oil price collapse after Saudi Arabia launched a price war. Oil prices experienced their worst quarter in history with prices dropping by close to 26% in the US on March 9 after Saudi Arabia dissolved a pact with Russia to curtail production. The prospect of reduced global demand due to COVID-19 forced the oil prices to enter in negative territory in April 2020 for the first time ever, as producers ran out of space to store the oversupply.

This rekindled fears for the solvency of the US shale industry from 2015/2016 when the world was last awash with oil. There was concern in markets then that there would be mass failures which would particularly rattle high yield bond markets. The worst concerns weren’t then realised but have re-emerged with COVID-19 and Saudi actions.

Investors are venturing out of safehaven assets

The deep recession in Q1 2020, fuelled by public health, economic, and energy crises, caused investors to start piling into expensive defensive and growth sectors like healthcare, information technology and consumer staples. In contrast, cyclical sectors such as banks, airlines, energy and travel stocks were hit hard.

As the economies went into hibernation to stop the spread of the coronavirus, major central banks slashed rates and restarted asset purchases, while G20 governments promised $5 trillion stimulus packages to moderate the economic impact of the pandemic. Such aggressive measures by policymakers globally boosted the safehaven assets such as government bonds and Gold. US Treasuries had their best quarter in Q2 2020 since the GFC and Gold price reached an all-time high of close to $2000/ounce in August 2020.

In Q2 2020, investors’ risk appetite gradually returned with the easing of COVID-19 lockdown restrictions and excessive monetary and fiscal stimulus measures announced across the world. This led to the recovery of equity markets with S&P 500 officially entering a bull market on August 18, reaching an all-time high of 3,500. While the S&P 500 index has returned to pre-pandemic levels, there is a sharp contrast in the gains of various sectors, with only 38% of stocks (primarily healthcare and information technology) in the index reporting gains over that period.

Which strategies worked?

Lonsec monitored a number of strategies within the global equities sector during the depths of the crisis that were deemed higher risk due to their market exposure, central bank or government policy intervention, market volatility, and illiquidity or possible high volumes of redemption requests.

While the market has now settled, we saw funds operating within hedged variation strategies, Emerging Markets, Quantitative, Natural Resources, and Fundamental Value, posting deep declines in the first quarter of 2020. Unsurprisingly, COVID-19 induced discrepancies in the wider sectors favoured growth managers over value (and the benchmark).

Value-style funds have endured a long period of underperformance relative to growth-biased peers in a long bull market favouring large technology firms. Lonsec notes that the Value managers under its coverage are not necessarily buying ‘junk’ stocks and that a volatile downturn such as this can be used as an opportunity to buy well-capitalised businesses at cheaper prices. While this sub-sector returned 3.7% for the June quarter, ranking at the lower end of the global equity spectrum, this remains a positive sign for those dogmatic value-oriented managers.

Lonsec notes that the funds management industry had been refocusing on systematic strategies which offer the promise of consistent and repeatable alpha but with scalability and cost advantages demanded by investors. Sadly, the average product in the Quantitative cohort experienced similar weakness to Fundamental Value due to a heavy dose of ‘value’ in addition to momentum in their quantitative models’ building blocks.

Quantitative strategies in general have struggled to price assets in current markets, as their processes are designed to function in ‘normal’ market conditions, when the market is operating according to fundamentals and long-term observations. The uncertainty, volatility, and leverage are causing pain generally across the sector. Performance for the average systematic product over Q1 2020 was -15.3%, compared to -3.0% per annum over the 12 months to 30 June 2020. Pleasingly, the average Managed-Volatility strategy outperformed its vanilla Quantitative peers, collectively returning -8.6% over the March quarter.

Typically emerging markets-oriented strategies tend to get caught up in a flight to quality, although Lonsec notes the Asia sub-sector (-7.6%) held up better than developed markets during Q1 2020 due in part to the relatively fast and well-organised response to COVID-19 within the region, presumably as a result of lessons learned in the past. The same cannot be said of regional India strategies (-20.8%), which suffered heavy losses given the country’s less successful containment efforts.

Other factors at play include the greater cyclical exposure generally within emerging market regions due to the greater exposure to commodities and energy from countries within the Latin America and Middle East regions, as well as Russia. As mentioned, dispersion has also considerably widened among stocks as the market punished companies exposed to discretionary spending (i.e. travel) and in highly cyclical sectors (i.e. energy), while rewarding those stocks that were unaffected or ended up benefiting from the new environment, most notably technology firms. Such dispersion is, however, an attractive environment for active managers to add considerable alpha.

Issued by Lonsec Research Pty Ltd ABN 11 151 658 561 AFSL 421 445 (Lonsec). Warning: Past performance is not a reliable indicator of future performance. Any advice is General Advice without considering the objectives, financial situation and needs of any person. Before making a decision read the PDS and consider your financial circumstances or seek personal advice. Disclaimer: Lonsec gives no warranty of accuracy or completeness of information in this document, which is compiled from information from public and third-party sources. Opinions are reasonably held by Lonsec at compilation. Lonsec assumes no obligation to update this document after publication. Except for liability which can’t be excluded, Lonsec, its directors, officers, employees and agents disclaim all liability for any error, inaccuracy, misstatement or omission, or any loss suffered through relying on the document or any information. ©2020 Lonsec. All rights reserved. This report may also contain third party material that is subject to copyright. To the extent that copyright subsists in a third party it remains with the original owner and permission may be required to reuse the material. Any unauthorised reproduction of this information is prohibited.