For consumers, 2019 was a year best forgotten as negative economic news created an almost perpetual drag on sentiment and global uncertainty resulted in repeated bouts of volatility. But for investors, including Australia’s 15 million super fund members, it was a year that saw a sizeable accumulation of wealth, driven by share market gains as well as some savvy investment decisions by the top-ranking funds.

Even with the high expectations set during a year that saw share markets rally ever higher, several super funds were able to translate this favourable environment into exceptional gains for members.

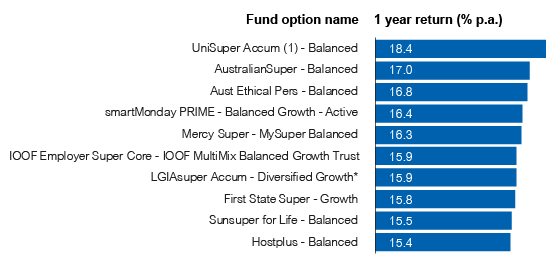

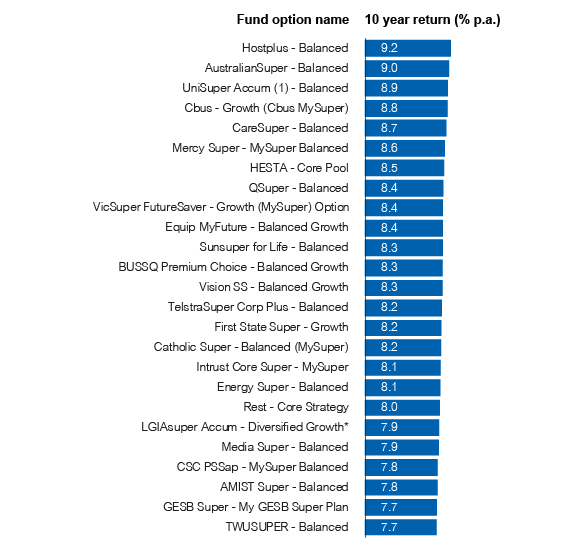

Topping the leader board in 2019 was UniSuper, whose balanced option delivered a return of 18.4% over the year and is among the top performers over 10 years with a return of 8.9% per annum. Over one year, UniSuper was followed by AustralianSuper – Australia’s largest fund – which returned 17.0% in 2019 and 9.0% over 10 years. However, it’s Hostplus that remains in first place over 10 years with an annual return of 9.2%.

Top 10 balanced options (return over 1 year)

*Interim return

Source: SuperRatings

Top 25 balanced options (return over 10 years)

*Interim return

Source: SuperRatings

UniSuper came out on top in a crowded field, in which the top 10 funds delivered an average return of 16.3%. It was a tight race over longer time periods, and while markets have certainly provided a tailwind, there’s no doubt that skilful management plays a role in squeezing out additional returns.

While returns may appear narrowly spread at the top, this hides some significant differences in asset allocation and investment strategies pursued by different funds. What was interesting to see was the diversity of approaches that funds take, even at the top of the leader board. While most funds have benefited from strong equity markets, the nuances among the top performers are where there has been strong value added for members.

In the case of UniSuper, the fund continues to pursue an active management strategy with exposures predominantly to Australian and International Equities, as well as significant cash and fixed interest exposures. Allocations to illiquid assets such as infrastructure and private equity are not a key component of their strategy.

Meanwhile, Hostplus has significant allocations to illiquid assets, with these being a key driver of its performance outcomes for Property, Infrastructure and Private Equity assets. AustralianSuper has also benefited from material unlisted asset exposures, as well as fee savings generated from its in-house investment structure.

Top pension funds

One of the key challenges super funds face is the current low-yield environment, which is making it harder for funds to generate income for members. This challenge is likely to be felt more acutely by those in the post-retirement phase, who rely on the income generated by their pension product to fund living expenses.

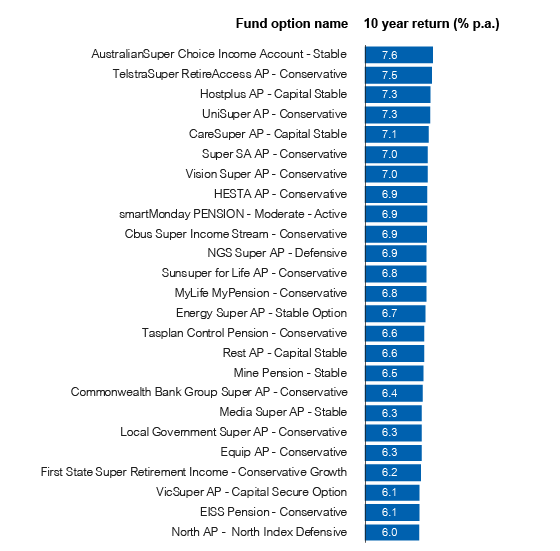

In this environment, picking the right pension fund and option can be critical. The below chart shows how capital stable pension options (20–40% growth assets) stack up over 10 years, and while there is some dispersion in the results, every option in the top 25 by performance exceeded the typical CPI plus 3.0% target. AustralianSuper’s Stable option is the best performer, returning 7.6% p.a. over ten years, followed closely by TelstraSuper’s Conservative option and Hostplus’s Capital Stable option.

Top 25 capital stable pension options (return over 10 years)

Source: SuperRatings

Understanding risk is critical for consumers

Most consumers can’t define risk, but they know it when they experience it. For superannuation members, risk can mean the likelihood of running out of money in retirement, or not having enough cash to pay for holidays, car repairs, or an inheritance for their kids.

For young members starting out in the workforce, short-term market falls might not matter too much because their investment horizon is relatively long. But for members nearing retirement, the timing of market ups and downs can have a significant effect on the wealth they have available in the drawdown phase.

For a young worker with a relatively low super balance, being exposed to riskier assets is less of a problem – in fact, it can help them accumulate wealth over their working life. However, for members approaching retirement (aged 50 and over), an unexpected pullback in the market can mean the difference between living comfortably and having to cut back in order to get by.

For this reason, it’s important to consider not only the return that a fund delivers but also the level of risk it takes on to achieve that return. In this context, risk means the degree of variability in returns over time. Growth assets like shares may return more on average than traditionally defensive assets like fixed income, but the range of return outcomes in a given period is greater.

The table below shows the top 25 funds ranked according to their risk-adjusted return, which measures how much members are being rewarded for taking on the ups and downs.

Top 25 balanced options based on risk and return

| Fund option name |

7 year return (% p.a.) |

Rank |

| QSuper – Balanced |

9.1 |

1 |

| CareSuper – Balanced |

9.8 |

2 |

| Cbus – Growth (Cbus MySuper) |

10.3 |

3 |

| Hostplus – Balanced |

10.5 |

4 |

| BUSSQ Premium Choice – Balanced Growth |

9.6 |

5 |

| Sunsuper for Life – Balanced |

10.0 |

6 |

| Catholic Super – Balanced (MySuper) |

9.4 |

7 |

| HESTA – Core Pool |

9.6 |

8 |

| CSC PSSap – MySuper Balanced |

9.0 |

9 |

| MTAA Super – My AutoSuper |

9.5 |

10 |

| Media Super – Balanced |

9.4 |

11 |

| Intrust Core Super – MySuper |

9.8 |

12 |

| AustralianSuper – Balanced |

10.5 |

13 |

| Mercy Super – MySuper Balanced |

10.0 |

14 |

| Rest – Core Strategy |

9.0 |

15 |

| First State Super – Growth |

9.7 |

16 |

| QANTAS Super Gateway – Growth |

8.3 |

17 |

| TWUSUPER – Balanced |

8.8 |

18 |

| Energy Super – Balanced |

9.3 |

19 |

| Local Government Super Accum – Balanced Growth |

9.0 |

20 |

| AMIST Super – Balanced |

8.9 |

21 |

| VicSuper FutureSaver – Growth (MySuper) Option |

9.8 |

22 |

| Club Plus Super – MySuper |

8.9 |

23 |

| NGS Super – Diversified (MySuper) |

8.9 |

24 |

| LGIAsuper Accum – Diversified Growth* |

8.9 |

25 |

Risk/return ranking determined by Sharpe Ratio

*Interim return

Source: SuperRatings

QSuper’s return of 9.1% p.a. over the past seven years is slightly below the average of 9.7% across the top 10 ranking funds, but it has the best return to risk ratio of its peers, meaning it delivered the best return given the level of risk involved. Funds such as CareSuper, Cbus and Hostplus were able to deliver higher returns, but for a slightly higher level of risk.