The past decade has seen managed accounts transform from a technologically viable but largely unexplored solution to one that is now fully embedded in financial advice models.

A key benefit of managed accounts is the efficiency they bring to financial advice practices. A large component of this efficiency relates to the fact that once a client is invested within a separately managed account structure there is no requirement for the financial adviser to issue a Record of Advice (RoA) when portfolio changes are made.

For the average advice firm with an average book size, this represents a serious advantage. Advisers can be high-energy individuals but contacting 80 clients every time a change is made to the portfolio is a tall order. Not only is it inefficient, but by the time the adviser is part way through the process of implementing the changes and notifying clients, market dynamics have changed, and previously identified investment opportunities have faded away.

This raises another significant advantage of managed accounts: responsiveness. Changes made to managed and SMA portfolios are instructed to all relevant platforms usually within two days after an investment committee has recommended a change. This means that advice clients can be aligned to the recommended portfolio structure almost immediately, allowing them to capture the full benefits of portfolio changes.

The advantage this provides for financial advisers and their clients goes beyond saving advisers time and making the process of portfolio implementation more efficient. Delays in implementation can cost clients investment upside, and in the long run can have a significant impact on investment performance and outcomes.

Measuring the cost of delay

While the cost of delayed implementation might seem like an academic issue, it isn’t. These costs are quantifiable, and they have a real impact on investment performance.

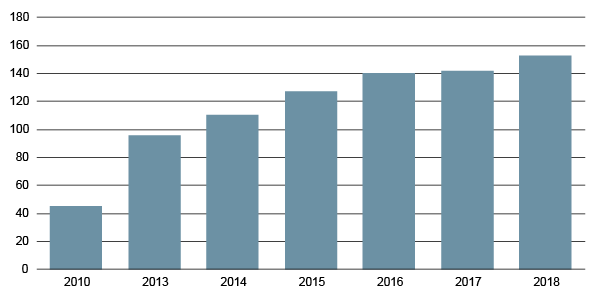

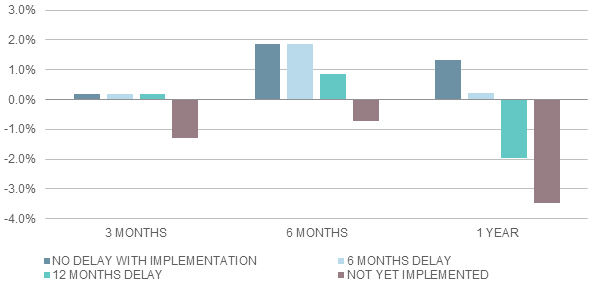

Lonsec conducted analysis using the Lonsec SMA – Australian Equities Core to illustrate the impact portfolio implementation delays can have on portfolio performance. The portfolio is an active concentrated portfolio investing in Australian listed equities. We have used actual portfolio changes recommended in December 2016 and then measured what the hypothetical excess return would look like over a three-month, six-month and one-year period under four implementation scenarios.

What these results show is that over a one-year period, implementing the portfolio changes with no delay resulted in an excess return of 1.3% above the benchmark S&P/ASX 200 Accumulation Index. This compares to an excess return of 0.2% with a six-month delay, a -2.0% excess return for a 12-month delay, and a -3.5% excess return if the portfolio change was not implemented.

Hypothetical excess return to March 2018 (delays to implement December 2016 portfolio changes)

Source: Lonsec

Responsive implementation allows clients to capture the full upside associated with changes in dynamic asset allocation and security selection. This is invaluable in an environment where the expectations of advice clients for actively managed, tailored and responsive portfolio management are growing. Increasingly, advisers need to be able to justify the costs involved in providing advice, and this means being able to show that their investment solutions are fit for purpose and able to respond nimbly to market opportunities in line with the client’s investment objectives.

Responsive, contemporary, active

Financial advisers can harness the managed account model to create a more efficient financial advice business and create more time to focus on the individual needs of clients. But often overlooked is the way in which responsive implementation enhances the value of the advice offering through better investment outcomes and by meeting the client’s expectations for active and timely management of their investments. This is where financial advice businesses can build a strong value proposition.

Meeting clients’ expectations in today’s advice world means meeting three criteria: responding market developments quickly, providing contemporary multi-asset portfolios, and actively managing and monitoring the client’s investment. In order to achieve this, advisers are increasingly turning to professional managed portfolio managers and SMA providers, outsourcing day-to-day portfolio management to an experienced team of investment consultants and focusing on providing holistic, goals-based advice.

By using Lonsec’s managed portfolios and SMA’s, advisers can access contemporary, actively managed multi-asset portfolios with dynamic asset allocation and active investment selection, backed by an investment committee comprising our senior investment consultants, research sector leads, and external economists.

This means investment solutions are backed by a highly qualified, well-resourced, and experienced group of investment professionals. They can also ensure their clients receive responsive and efficient implementation of investment decisions, avoiding delays that can eat into investment performance while winning back time to build enduring client relationships with an appropriate level of service.

Important Notice: This document is published by Lonsec Investment Solutions Pty Ltd ACN: 608 837 583, a corporate authorised representative (CAR number: 1236821) (LIS) of Lonsec Research Pty Ltd ABN: 11 151 658 561 AFSL: 421 445 (Lonsec Research)). LIS creates the model portfolios it distributes using the investment research provided by Lonsec Research but has not had any involvement in the investment research process for Lonsec Research. LIS and Lonsec Research are owned by Lonsec Holdings Pty Ltd ACN: 151 235 406. Please read the following before making any investment decision about any financial product mentioned in this document.

Disclosure at the date of publication: Lonsec Research receives a fee from the relevant fund manager or product issuers for researching financial products (using objective criteria) which may be referred to in this document. Lonsec Research may also receive a fee from the fund manager or product issuer (s) for subscribing to research content and other Lonsec Research services. Lonsec Research receives fees for providing investment consulting advice, approved product lists and other advice, to clients. LIS receives a fee for providing the model portfolios to financial services professionals. LIS’ and Lonsec Research’s fees are not linked to the financial product rating(s) outcome or the inclusion of the financial product(s) in model portfolios. LIS and Lonsec Research may hold any financial product(s) referred to in this document. Lonsec Research’s representatives and/or their associates may hold any financial product(s) referred to in this document, but details of these holdings are not known to the analyst(s).

Warnings: Past performance is not a reliable indicator of future performance. Any express or implied rating or advice presented in this document is limited to “general advice” (as defined in the Corporations Act 2001 (Cth)) and based solely on consideration of the investment merits of the financial product(s) alone, without taking into account the investment objectives, financial situation and particular needs (“financial circumstances”) of any particular person. Before making an investment decision based on the rating or advice, the reader must consider whether it is personally appropriate in light of his or her financial circumstances or should seek independent financial advice on its appropriateness. If the advice relates to the acquisition or possible acquisition of a particular financial product, the reader should obtain and consider the Investment Statement or the Product Disclosure Statement for each financial product before making any decision about whether to acquire the financial product.

Disclaimer: LIS provides this document for the exclusive use of its clients. It is not intended for use by a retail client or a member of the public and should not be used or relied upon by any other person. No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented in this document, which is drawn from public information not verified by LIS. Financial conclusions, ratings and advice are given on reasonable grounds held at the time of completion (refer to the date of this document) but subject to change without notice. LIS assumes no obligation to update this document following publication. Except for any liability which cannot be excluded, LIS and Lonsec, their directors, officers, employees and agents disclaim all liability for any error or inaccuracy in, misstatement or omission from, this document or any loss or damage suffered by the reader or any other person as a consequence of relying upon it.

Copyright © 2018 Lonsec Investment Solutions Pty Ltd ACN: 608 837 583 (LIS), a corporate authorised representative (CAR number: 1236821) of Lonsec Research Pty Ltd ABN: 11 151 658 561 AFSL: 421 445 (Lonsec Research). This report is subject to copyright of LIS. Except for the temporary copy held in a computer’s cache and a single permanent copy for your personal reference or other than as permitted under the Copyright Act 1968 (Cth), no part of this report may, in any form or by any means (electronic, mechanical, micro-copying, photocopying, recording or otherwise), be reproduced, stored or transmitted without the prior written permission of LIS.

This report may also contain third party supplied material that is subject to copyright. Any such material is the intellectual property of that third party or its content providers. The same restrictions applying above to LIS copyrighted material, applies to such third-party content.