Is it time for retirees to batten down the hatches? And mitigate losses happening at the worst possible time.

Australian Investors have witnessed a 10-year bull run in Equities, and a near 30-year bull run in bonds and house values. But just as the middle Baby Boomers retire at the peak of

their wealth, headwinds are whipping up against all three of the main asset classes they’re invested in. Retirees would be wise to consider allocating a portion of their wealth to safe

harbours at this point in the retirement journey, when losses will be difficult to recoup.

How do I identify a safe harbour?

There is an eternal trade-off between risk & return. When reducing risk, a reduction in return should be expected. When approaching retirement an investor should consider whether it’s appropriate to dial down their exposure to riskier asset classes. They should also be looking to invest a portion of their wealth in asset classes which behave differently, ideally independently, to their existing investments.

Right now, we’re in an unusual period where equity, fixed income AND the family home are at historically high valuations simultaneously. Cash, in the form of bank deposits, is an

alternative to these investments – but at current interest rates inflation may gradually erode the value. Is it time to look to alternative investments which keep up with, and exceed,

inflation?

Alternatives, global direct real estate and senior secured loans generally benefit in an inflationary environment. They are generally out-of-synch with equities and bonds, but it’s not guaranteed. Therefore, an option may be to invest in a fund which is specifically designed to be out-of-synch with equities and bonds, as well as capture returns which keep ahead of inflation.

1st rule of investing: don’t make losses

2nd rule of investing: see above, especially near retirement

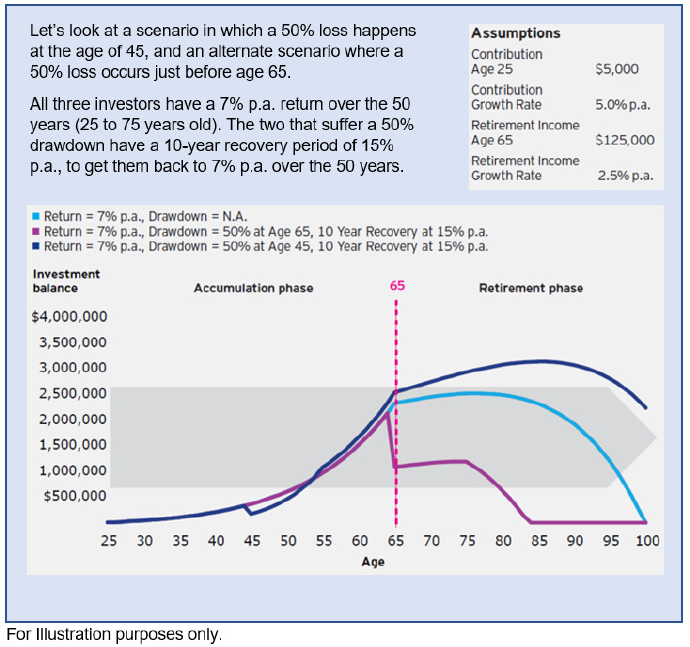

The day of retirement is when an individual’s investments are generally at their peak. It is also when the consequences of losses are most acute. This is because large losses at this

point will be very difficult to recoup. For example, a 45-year-old who incurs large portfolio losses typically has 20 years before reaching retirement, and therefore has a long time horizon

over which to recover losses. The situation is very different when a 65-year-old incurs large losses. Such losses may undermine the quality of the retirement that was anticipated, they may delay retirement, or they may even force a retiree back to work.

Ashley O’Connor is the Head of Investment Strategy at Invesco Australia. He has a Bachelor of Commerce and was previously the Head of Debt at Frontier Advisors.

Important information

This document has been prepared by Invesco Australia Ltd (Invesco) ABN 48 001 693 232, Australian Financial Services Licence number 239916, who can be contacted on freecall 1800 813 500, by email to info@au.invesco.com, or by writing to GPO Box 231, Melbourne, Victoria, 3001. You can also visit our website at www.invesco.com.au

This document contains general information only and does not take into account your individual objectives, taxation position, financial situation or needs. You should assess whether the information is appropriate for you

and consider obtaining independent taxation, legal, financial or other professional advice before making an investment decision. A Product Disclosure Statement (PDS) for any Invesco fund referred to in this document is available from Invesco. You should read the PDS and consider whether a fund is appropriate for you before making a decision to invest.

Invesco is authorised under its licence to provide financial product advice, deal in financial products and operate registered managed investment schemes. If you invest in an Invesco Fund, Invesco may receive fees in relation

to that investment. Details are in the PDS. Invesco’s employees and directors do not receive commissions but are remunerated on a salary basis. Neither Invesco nor any related corporation has any relationship with other product issuers that could influence us in providing the information contained in this document.

Investments in the Invesco funds are subject to investment risks including possible delays in repayment and loss of income and principal invested. Neither Invesco nor any other member of the Invesco Ltd Group guarantee the return of capital, distribution of income, or the performance of any of the Funds. Any investments in the Funds do not represent deposits in, or other liabilities of, any other member of the Invesco Ltd Group.

Invesco has taken all due care in the preparation of this document. To the maximum extent permitted by law, Invesco, its related bodies corporate, directors or employees are not liable and take no responsibility for the accuracy or completeness of this document and disclaim all liability for any loss or damage of any kind (whether foreseeable or not) that may arise from any person acting on any statements contained in this document. This document has been prepared only for those persons to whom Invesco has provided it. It should not be relied upon by anyone else.

©Copyright of this document is owned by Invesco. You may only reproduce, circulate and use this document (or any part of it) with the consent of Invesco.