With half the country in what seems never ending rounds of lockdowns and pandemic fatigue setting in, one of the last things most Australians want to do is look at their Superannuation balances and investment options. That is, however, exactly what SuperRatings is wanting us to do, as neglecting your super or responding to short term market moves can have a detrimental effect on your super balance.

SuperRatings Executive Director Kirby Rappell says, ‘We looked at the impact of switching out of a balanced or growth option and into cash at the start of the pandemic and found that those with a balance of $100,000 in January 2020 and who switched to cash at the end of March would now be around $22-27,000 worse off than if they had not switched.’

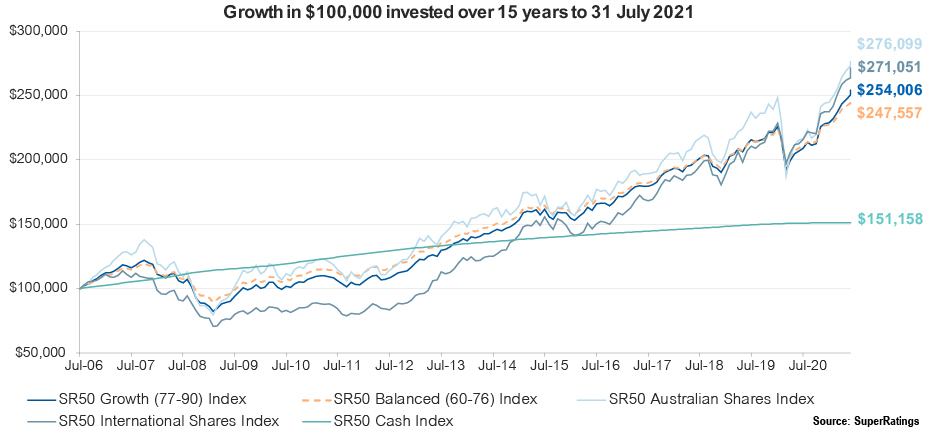

This effect of switching into cash as a response to market turmoil is also seen when looking at returns over the past 15 years. In this period, a typical balanced Super option has risen substantially, with a balance of $100,000 in July 2006 accumulating to $247,557, more than doubling in size. Those members investing in a growth option have experienced an even stronger result, with a similar starting balance growing to $254,006. Share focused options have delivered the highest returns, with the median Australian shares option growing to $276,099 and the median international shares option growing to $271,051, though these types of options involve greater risks. Over the same period, a $100,000 balance invested in cash would only be worth $151,158 today.

When considering your Super options, you don’t need to go it alone as many Super funds provide advice and tools to their members. Says Mr Rappell, ‘Most funds will offer scaled advice for free or at a low cost, with members able to get advice on topics such as contributions, investment options, insurance in the fund and the transition to retirement.’ Scaled advice is general in nature so you will need to check if your situation and goals align with the advice.

Continues Mr Rappell, ‘For members who want more tailored advice, some funds will offer comprehensive advice that will also take into account your financial assets outside of superannuation.’ While there will be a cost associated with this comprehensive advice, most funds will allow the cost of the advice to be deducted from the superannuation account, just make sure you check any costs and how they can be paid before agreeing to get the advice.

Looking at more recent returns, balances continued to grow in July. The typical balanced option returned an estimated 1.3% over the month and 18.5% over the year. The typical growth option returned an estimated 1.3% for the month and the median capital stable option also increased 0.9% in the month.

Accumulation returns to July 2021

| FYTD | 1 yr | 3 yrs (p.a.) | 5 yrs (p.a.) | 7 yrs (p.a.) | 10 yrs (p.a.) | |

|---|---|---|---|---|---|---|

| SR50 Balanced (60-76) Index | 1.3% | 18.5% | 7.9% | 8.4% | 8.0% | 8.6% |

| SR50 Capital Stable (20-40) Index | 0.9% | 7.8% | 4.5% | 4.5% | 4.8% | 5.3% |

| SR50 Growth (77-90) Index | 1.3% | 22.7% | 9.2% | 9.5% | 8.9% | 9.6% |

Source: SuperRatings estimates

Pension returns were also positive in July. The median balanced pension option returned an estimated 1.3% over the month and 20.0% over the year. The median pension growth option returned an estimated 1.5% and the median capital stable option also rose an estimated 0.9% in the month.

Pension returns to July 2021

| FYTD | 1 yr | 3 yrs (p.a.) | 5 yrs (p.a.) | 7 yrs (p.a.) | 10 yrs (p.a.) | |

|---|---|---|---|---|---|---|

| SRP50 Balanced (60-76) Index | 1.3% | 20.0% | 8.4% | 9.1% | 8.5% | 9.5% |

| SRP50 Capital Stable (20-40) Index | 0.9% | 8.6% | 5.2% | 5.2% | 5.2% | 5.9% |

| SRP50 Growth (77-90) Index | 1.5% | 24.4% | 9.7% | 10.3% | 9.8% | 10.6% |

Source: SuperRatings estimates

Release ends

Warnings: Past performance is not a reliable indicator of future performance. Any express or implied rating or advice presented in this document is limited to “General Advice” (as defined in the Corporations Act 2001(Cth)) and based solely on consideration of the merits of the superannuation or pension financial product(s) alone, without taking into account the objectives, financial situation or particular needs (‘financial circumstances’) of any particular person. Before making an investment decision based on the rating(s) or advice, the reader must consider whether it is personally appropriate in light of his or her financial circumstances, or should seek independent financial advice on its appropriateness. If SuperRatings advice relates to the acquisition or possible acquisition of particular financial product(s), the reader should obtain and consider the Product Disclosure Statement for each superannuation or pension financial product before making any decision about whether to acquire a financial product. SuperRatings research process relies upon the participation of the superannuation fund or product issuer(s). Should the superannuation fund or product issuer(s) no longer be an active participant in SuperRatings research process, SuperRatings reserves the right to withdraw the rating and document at any time and discontinue future coverage of the superannuation and pension financial product(s).

Copyright © 2021 SuperRatings Pty Ltd (ABN 95 100 192 283 AFSL No. 311880 (SuperRatings)). This media release is subject to the copyright of SuperRatings. Except for the temporary copy held in a computer’s cache and a single permanent copy for your personal reference or other than as permitted under the Copyright Act 1968 (Cth.), no part of this media release may, in any form or by any means (electronic, mechanical, micro-copying, photocopying, recording or otherwise), be reproduced, stored or transmitted without the prior written permission of SuperRatings. This media release may also contain third party supplied material that is subject to copyright. Any such material is the intellectual property of that third party or its content providers. The same restrictions applying above to SuperRatings copyrighted material, applies to such third party content.