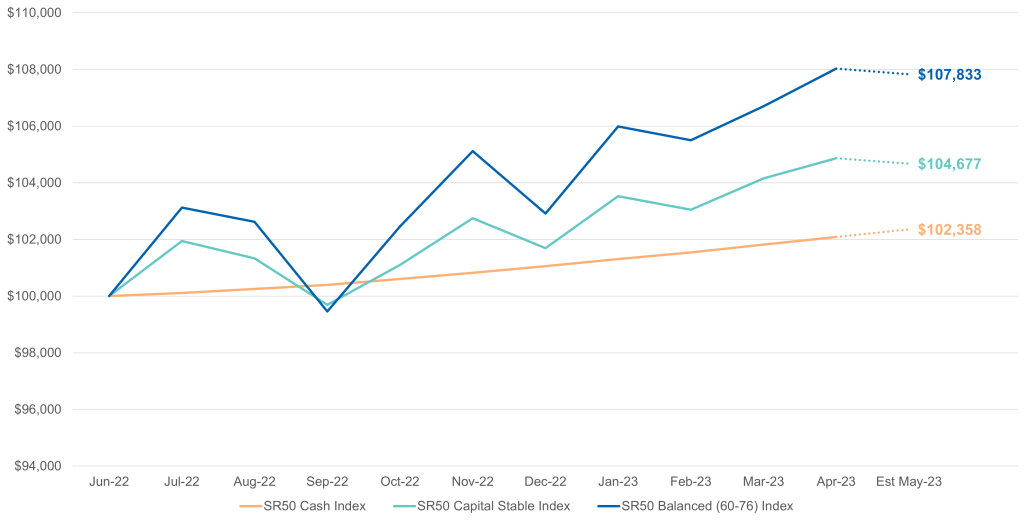

After a positive start to the new financial year, super fund returns faced modest headwinds in August with the median balanced option delivering an estimated return of -0.1% according to leading superannuation research house SuperRatings.

The trajectory for inflation remains a key driver for markets with uncertainty around central bank’s rates pathway remaining front of mind. Both Australian and global equities reported small declines over the month with diversification continuing to benefit members in reducing underperformance.

The median growth option fell by an estimated -0.3%, while lower exposure to shares resulted in the median capital stable option delivering a small positive result, with an increase of 0.1% for August.

Accumulation returns to August 2023

| Monthly | 1 yr | 3 yrs (p.a.) |

5 yrs (p.a.) |

7 yrs (p.a.) |

10 yrs (p.a.) |

|

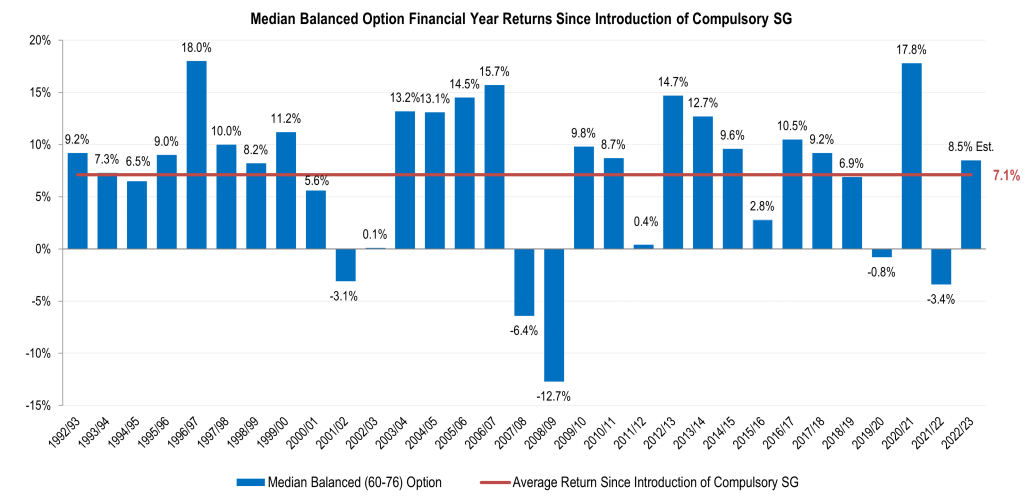

| SR50 Balanced (60-76) Index | -0.1% | 7.7% | 7.1% | 5.7% | 6.6% | 7.2% |

| SR50 Capital Stable (20-40) Index | 0.1% | 4.2% | 3.0% | 3.1% | 3.6% | 4.5% |

| SR50 Growth (77-90) Index | -0.3% | 9.3% | 8.5% | 6.6% | 8.1% | 8.4% |

Source: SuperRatings estimates

Pension returns followed a similar trend over the month, with the median balanced pension option falling an estimated -0.1%. The median growth option is estimated to decline -0.2% in August while the more defensive median capital stable pension option is estimated to deliver a 0.1% gain.

Pension returns to August 2023

| Monthly | 1 yr | 3 yrs (p.a.) |

5 yrs (p.a.) |

7 yrs (p.a.) |

10 yrs (p.a.) |

|

| SR50 Balanced (60-76) Index | -0.1% | 8.7% | 7.7% | 6.3% | 7.5% | 7.9% |

| SR50 Capital Stable (20-40) Index | 0.1% | 4.7% | 3.4% | 3.4% | 4.1% | 4.9% |

| SR50 Growth (77-90) Index | -0.2% | 9.8% | 9.1% | 7.4% | 8.9% | 9.2% |

Source: SuperRatings estimates

“Market uncertainty persists, and we continue to expect monthly fund returns to bounce around” commented Executive Director of SuperRatings, Kirby Rappell, “However, over the long term, we know funds have a strong record of performing above objectives. The key message for most members is ensuring their settings are right for the long term in order to provide dignity in retirement.”

Monitoring investment performance is a good hygiene factor for members and the results of the latest annual performance test were recently released. The test has had a significant impact on MySuper default products over the past three years with the only MySuper product to fail the test this year already being closed to new members. The test was also expanded to a broader range of products this year and members who are invested in a failing product will soon be receiving a letter from their fund. If you do receive that letter, make sure you review your investment option or speak with a trusted adviser to understand why it failed and if it’s still suitable for you.

“We’ve seen a more subdued return for super funds over August, however the strong returns in July mean performance remains positive overall for the new financial year. We encourage members to focus on the longer term and be prepared to see more ups and downs over the coming months” concluded Mr Rappell.

Release ends

We welcome media enquiries regarding our research or information held in our database. We are also able to provide commentary and customised tables or charts for your use.

For more information contact:

Kirby Rappell

Executive Director

Tel: 1300 826 395

Mob: +61 408 250 725

Kirby.Rappell@superratings.com.au