There is a powerful maxim best suited to the current predicament faced by markets, and that is, there are decades where nothing happens, and there are weeks where decades happen. The advent of 2020 has brought with it unprecedented volatility, with markets whipsawing erratically and appearing to have detached completely from the underlying fundamentals. No sooner had investors been beaten into submission from depression era plunges in equity markets, were they then riding a jubilant wave of euphoria on a spectacular relief rally. Unfortunately, there is no investing rule book which outlines how to effectively manoeuvre your portfolio while the global economy is placed in suspended animation and a deadly viral pathogen wreaks havoc. However, if there was ever an opportunity for active investing to shine, this is it.

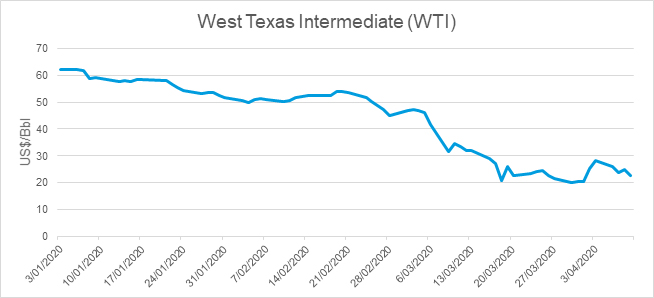

In the midst of a lethal pandemic gripping markets, investors have also been dealt a one-two punch of a brutal collapse in oil prices amid a price war between Saudi Arabia and Russian. As such, the price of West Texas Intermediate (WTI) has plummeted from US$62/bbl to a low of US$20/bbl, and now seriously threatens the viability of a highly leveraged global energy industry. While lower oil prices translate into lower transportation costs, this is less relevant given large swathes of the globe are in lockdown and the airline industry has drastically curbed output.

Source: Bloomberg

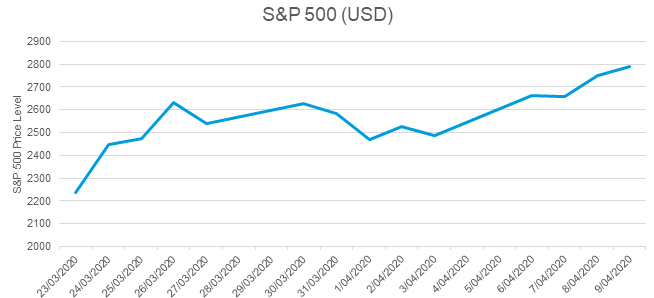

Importantly, with the price of oil well below break-even, exploration and production will come to a standstill and untold numbers of jobs will be lost. Bizarrely however, in a market gripped by panic, the mindset has inexplicably shifted from selling anything (barring safe-haven currencies and US Treasuries) to a dramatic reversal bordering on irrational exuberance. This is perfectly exemplified by the FOMO (fear-of-missing-out) driven bull market rally, where investors are piling in despite the IMF now predicting the deepest economic downturn since the Great Depression of the 1930s. Astoundingly, the S&P 500 has now notched a 25% return from the depths of the recent bear-market low.

Source: Bloomberg

So, this leaves the pundits questioning, has a technical bottom been found in the markets, or are we witnessing a textbook bear-market rally? In the case of the former, perhaps it’s the invisible hand of the market looking through to a solid economic and corporate upturn. Conversely however, the rally could simply be driven by over-optimism around global governments and central banks being ‘all-in’ amid past condition to ‘buy-the-dip’. Given the magnitude of the uncertainties we’re faced with, intuition favours the latter. This has tended to be the consensus view held among Australian equity portfolio managers when posing the same question during meetings as part of Lonsec’s annual review process over the course of the first two weeks of April. Moreover, some Managers are bearishly predicting a re-test of the lows experienced in March.

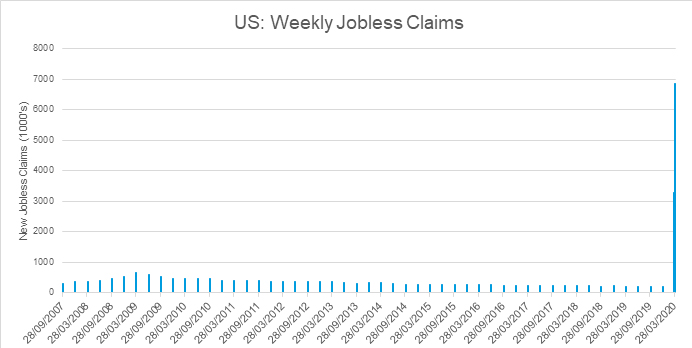

Historically, downward trending bear markets have frequently been plagued with sharp relief rallies, only to run out of steam and reverse course. Logic likely dictates that given the magnitude of the deteriorating fundamentals and economic data, a sustained recovery from here is likely over-optimistic. This was evidenced throughout the latter stages of 2008 where the S&P 500 was in the grips of a death-spiral despite numerous surges ranging from 10-25%, to ultimately bottom in March 2009. Furthermore, if using weekly jobless claims in the US as a proxy for the health of the global economy, the outlook appears dire. Jobless claims continue to skyrocket and take the cumulative total number of people who have lost their job since March 2020 to almost 17 million. In the singular month of March these jobless claims have already far outstripped the devastation witnessed during the Great Recession of 2008.

The dislocation in the credit markets has likewise been pronounced, and counterintuitively, this has spread to sovereign bonds which are typically immune from indiscriminate selling. Perversely, the US Federal Reserve has resorted to not only purchasing sovereign debt, but also sub-investment grade bonds through high-yield credit ETFs. In a sign of how distorted capital markets have come, the Fed is now extending credit to cash-starved corporates in attempts to stymie a systemic economic contagion in which credit markets freeze and liquidity evaporates. Once again, this type of intervention is without precedent and has significantly stabilised markets through keeping these companies on life-support whilst the ‘risk-off’ sentiment remains heightened. However, both credit spreads and trading in credit default swaps (CDS) remain elevated which suggests a marked disconnect between the ‘blue-sky’ scenario priced into equity markets, and fixed income securities languishing in the doldrums. Consequently, in the face of such ghastly economic data, one would imagine that the ‘Fed-Put’ is starting to weaken. Alternatively, perhaps we’re witnessing the last vestiges of blood being wringed from the retail investors with quantitative trading driving momentum higher before a swift ‘pump and dump’ ensues. So, for those telling themselves that this time is different, a word of caution, as history does not repeat itself, but it does rhyme.

Source: Bloomberg

The global economy is now likely wrestling with a complete paradigm shift in how globalisation is viewed. The longer we remain in lockdown limbo, the greater the push will be for a secular and structural de-globalisation of the world economy in the post-crisis landscape. Not only has the world been devastated through the effects of a global health catastrophe, but Orwellian impositions on our personal liberties have been thrust upon us that would have been utterly inconceivable barely months ago. Moreover, the chasm between the ‘haves’ and the ‘have-nots’ has radically deepened as a wider dispersion between the working class and the inner-city elites has been exposed. Given the increasing social unrest we’ve already witnessed unravelling in supermarkets, it’s not a stretch to see this playing out on a broader scale. Likewise, the America First mantra now appears less xenophobic as countless other countries have adopted even more radical shifts to protectionism in a fight to survive. A likely consequence of this would be the return of innovation and manufacturing to many countries, where previously this function had been outsourced to China. Case in point being the world’s reliance on China for life-saving pharmaceuticals. Australia imports approximately 90% of medicines, where an outsized reliance is placed on China to meet these needs. As such, given the supply chain vulnerabilities exposed by COVID-19, a re-assessment of Australia’s sovereign capability to meet our domestic pharmaceutical consumption is warranted. Secondly, corporate vanity and window dressing will likely take the back seat as companies are forced to re-focus on their core stakeholders when staring down the barrel of economic ruin.

The exogenous COVID-19 shock has exposed significant vulnerabilities in the financial system yet has also created potentially lucrative investment opportunities for rational investors. Whilst it might be difficult to maintain a dispassionate outlook at this juncture, remember that it isn’t the end, and that markets will bottom well in advance of a positive shift in investor sentiment. If history is anything to go by, you should never let a good crisis go to waste and use this opportunity to dollar-cost-average, as this could be our March 2009 moment. With that said however, the market always delights in humbling the masses, so proceed with caution.