Super funds have started the new financial year with some positive momentum but face a period of stark uncertainty as Australian cases of Covid-19 rise and Victoria enters harsher lockdown conditions.

While we have seen stabilisation in markets, they remain vulnerable to further shocks, while super fund performance is contingent on how communities and economies cope with further waves of infections.

According to estimates from leading superannuation research house SuperRatings, the median balanced option returned 0.9% in July as markets continued to rebuild following March’s falls. Overall, super funds have made it through in good shape but are preparing for more market ups and downs through the rest of the 2020 calendar year.

“The outlook is still unclear but based on recent performance super funds have shown they can weather the Covid-19 storm,” said SuperRatings Executive Director Kirby Rappell.

“Looking at SuperRatings’ balanced option index, the sector is 4.0% below where it was at the start of 2020. This is less than ideal for members, but thanks to the recovery we saw over the June quarter we have already made up a lot of ground. Hopefully this momentum can continue, and members can swiftly regain their super wealth.”

According to SuperRatings’ estimates, the median balanced option is down 1.2% over the 12 months to July. The median growth option is estimated to have fallen -1.7% while the median capital stable option is steady at 0.5%.

Accumulation returns to end of July 2020

| CYTD | 1 yr | 3 yrs (p.a.) | 5 yrs (p.a.) | 7 yrs (p.a.) | 10 yrs (p.a) | |

| SR50 Growth (77-90) Index | -5.1% | -1.7% | 5.8% | 5.9% | 7.7% | 7.8% |

| SR50 Balanced (60-76) Index | -4.0% | -1.2% | 5.5% | 5.3% | 6.9% | 7.4% |

| SR50 Capital Stable (20-40) Index | -0.9% | 0.5% | 3.7% | 3.8% | 4.6% | 5.1% |

Source: SuperRatings estimates

Pension returns have performed more or less in line with accumulation returns over the past year. The median balanced pension option is estimated to have fallen 1.2% over the 12 months to July, compared to a drop of 1.9% from the median growth option and a modest rise of 0.5% from the median capital stable option.

Pension returns to end of July 2020

| CYTD | 1 yr | 3 yrs (p.a.) | 5 yrs (p.a.) | 7 yrs (p.a.) | 10 yrs (p.a) | |

| SRP50 Growth (77-90) Index | -5.6% | -1.9% | 6.5% | 6.7% | 8.5% | 8.7% |

| SRP50 Balanced (60-76) Index | -4.1% | -1.2% | 6.0% | 6.0% | 7.5% | 8.1% |

| SRP50 Capital Stable (20-40) Index | -1.0% | 0.5% | 4.3% | 4.3% | 5.1% | 5.8% |

Source: SuperRatings estimates

July’s results represent the fourth month in a row of positive returns for super, following the 9.2% drop members experienced in March. While the results are promising, there is still a way to go before members recoup their losses, and the Covid-19 situation in Australia remains precarious as other states brace for potential spikes in infections.

“We can certainly take heart from recent performance, but we should not underestimate the challenge that we still face,” said Mr Rappell.

“Markets are incredibly difficult to navigate at the moment. Globally, we are seeing a disconnect between the rise in share valuations and the weakness in economic data. Meanwhile, the low yield environment will only be exacerbated by governments issuing more debt to shore up budgets and continue providing support to those affected by the virus.”

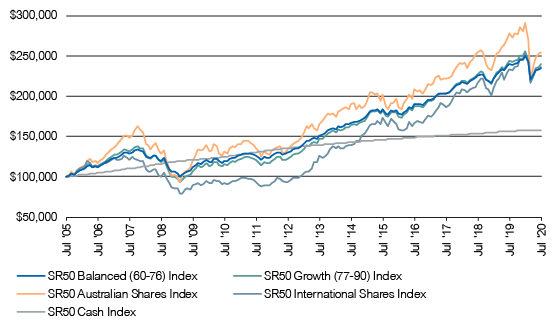

Growth in $100,000 invested over 15 years to 30 July 2020

Source: SuperRatings estimates

Taking a long-term view, super returns have done an incredible job at accumulating wealth for retirees over a period that includes two major financial and economic crises. According to SuperRatings’ data, since July 2005, a starting balance of $100,000 would now be worth $235,877 for members in a balanced option. For a growth option this would be slightly higher at $236,235. A member with full exposure to Australian shares would have seen their balance growth to $254,188. In contrast, returns on cash would have seen the balance grow to only $157,939.